《计算机应用》唯一官方网站 ›› 2022, Vol. 42 ›› Issue (8): 2326-2332.DOI: 10.11772/j.issn.1001-9081.2021061053

• 人工智能 • 上一篇

Minghui WU1( ), Guangjie ZHANG1,2, Canghong JIN1

), Guangjie ZHANG1,2, Canghong JIN1

摘要:

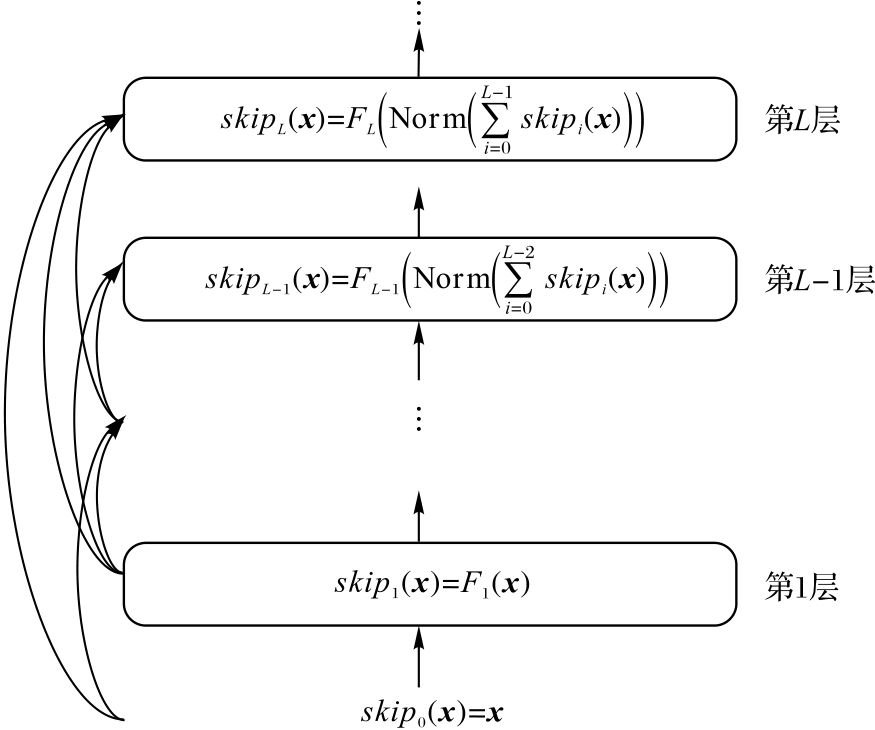

针对传统单因子模型无法充分利用时间序列相关信息,以及这些模型对时间序列预测准确性和可靠性较差的问题,提出一种基于多模态信息融合的时间序列预测模型——Skip-Fusion对多模态数据中的文本数据和数值数据进行融合。首先利用BERT(Bidirectional Encoder Representations from Transformers)预训练模型和独热编码对不同类别的文本数据进行编码表示;再使用基于全局注意力机制的预训练模型获得多文本特征融合的单一向量表示;然后将得到的单一向量表示与数值数据按时间顺序对齐;最后通过时间卷积网络(TCN)模型实现文本和数值特征的融合,并通过跳跃连接完成多模态数据的浅层和深层特征的再次融合。在股票价格序列的数据集上进行实验,Skip-Fusion模型的均方根误差(RMSE)和日收益(R)分别为0.492和0.930,均优于现有的单模态模型和多模态融合模型的结果,同时在可决系数(R-Squared)上取得了0.955的拟合优度。实验结果表明,Skip-Fusion模型能够有效进行多模态信息融合并具有较高的预测准确性和可靠性。

中图分类号: