Journal of Computer Applications ›› 2023, Vol. 43 ›› Issue (5): 1378-1384.DOI: 10.11772/j.issn.1001-9081.2022030400

• China Conference on Data Mining 2022 (CCDM 2022) • Previous Articles

Yafei ZHANG1,2,3, Jing WANG1,2,3, Yaoshuai ZHAO3,4( ), Zhihao WU1,2,3, Youfang LIN1,2,3

), Zhihao WU1,2,3, Youfang LIN1,2,3

Received:2022-03-30

Revised:2022-05-17

Accepted:2022-05-26

Online:2023-05-08

Published:2023-05-10

Contact:

Yaoshuai ZHAO

About author:ZHANG Yafei, born in 1997, M. S. candidate. His research interests include data mining, machine learning.Supported by:

张亚飞1,2,3, 王晶1,2,3, 赵耀帅3,4(), 武志昊1,2,3, 林友芳1,2,3

通讯作者:

赵耀帅

作者简介:张亚飞(1997—),男,河北邢台人,硕士研究生,主要研究方向:数据挖掘、机器学习基金资助:CLC Number:

Yafei ZHANG, Jing WANG, Yaoshuai ZHAO, Zhihao WU, Youfang LIN. Stock movement prediction with market dynamic hierarchical macro information[J]. Journal of Computer Applications, 2023, 43(5): 1378-1384.

张亚飞, 王晶, 赵耀帅, 武志昊, 林友芳. 融合市场动态层次宏观信息的股票趋势预测[J]. 《计算机应用》唯一官方网站, 2023, 43(5): 1378-1384.

Add to citation manager EndNote|Ris|BibTeX

URL: http://www.joca.cn/EN/10.11772/j.issn.1001-9081.2022030400

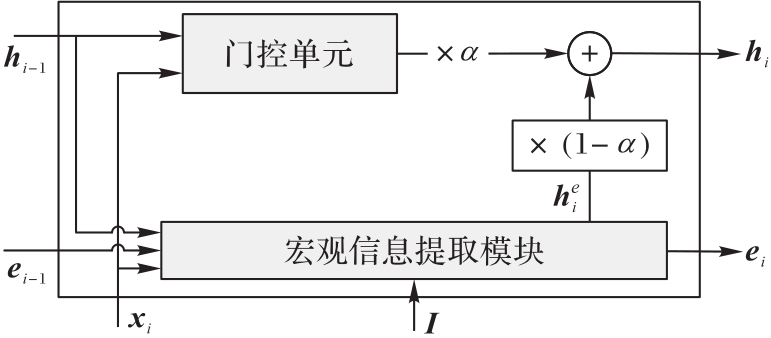

Fig.1 Architecture of DMMN

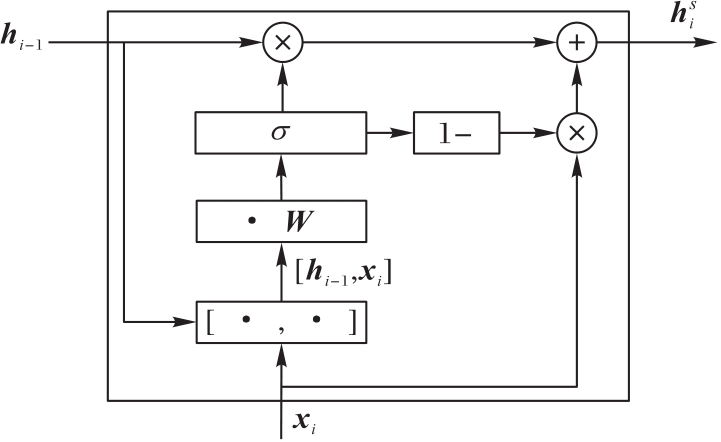

Fig.2 Macro memory unit

Fig. 3 Gated unit

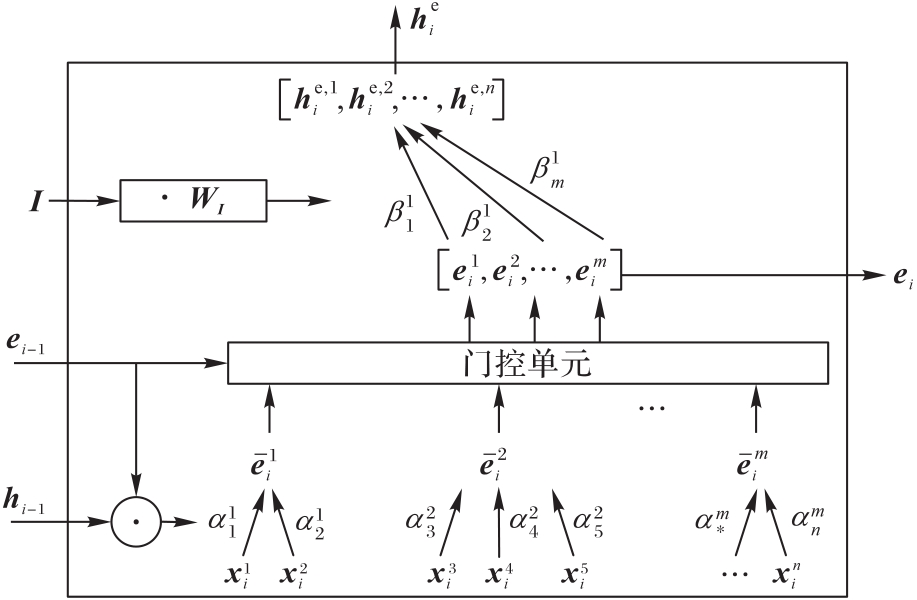

Fig. 4 Macro information extraction module for stock market

| 数据段 | 开始日期 | 结束日期 | 股票数 | 行业数 | 样本数 | l1/% | l2/% |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-18 | 2011-09-07 | 177 | 65 | 70 800 | -0.847 1 | 0.804 8 |

| 2 | 2012-01-30 | 2013-09-18 | 219 | 68 | 87 600 | -0.746 4 | 0.727 3 |

| 3 | 2014-02-24 | 2015-10-13 | 231 | 69 | 92 400 | -0.781 5 | 1.052 6 |

| 4 | 2016-03-10 | 2017-10-27 | 250 | 70 | 100 000 | -0.521 1 | 0.517 6 |

| 5 | 2018-03-27 | 2019-11-15 | 272 | 73 | 108 800 | -0.780 4 | 0.691 4 |

Tab. 1 Data description

| 数据段 | 开始日期 | 结束日期 | 股票数 | 行业数 | 样本数 | l1/% | l2/% |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-18 | 2011-09-07 | 177 | 65 | 70 800 | -0.847 1 | 0.804 8 |

| 2 | 2012-01-30 | 2013-09-18 | 219 | 68 | 87 600 | -0.746 4 | 0.727 3 |

| 3 | 2014-02-24 | 2015-10-13 | 231 | 69 | 92 400 | -0.781 5 | 1.052 6 |

| 4 | 2016-03-10 | 2017-10-27 | 250 | 70 | 100 000 | -0.521 1 | 0.517 6 |

| 5 | 2018-03-27 | 2019-11-15 | 272 | 73 | 108 800 | -0.780 4 | 0.691 4 |

| 数据段 | F1分数 | 夏普比率 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ARIMA | MLP | CNN | LSTM | GCN-LSTM | ALSTM | DMMN | ARIMA | MLP | CNN | LSTM | GCN-LSTM | ALSTM | DMMN | |

| 1 | 0.230 3 | 0.166 3 | 0.343 8 | 0.343 2 | 0.353 9 | 0.392 2 | -0.005 2 | -0.005 2 | 0.066 9 | 0.060 3 | -0.045 3 | 0.057 2 | ||

| 2 | 0.213 8 | 0.171 6 | 0.284 8 | 0.365 6 | 0.346 3 | 0.409 2 | -0.003 0 | -0.003 0 | 0.008 8 | 0.041 2 | -0.049 2 | 0.172 1 | ||

| 3 | 0.219 5 | 0.198 4 | 0.274 3 | 0.385 6 | 0.364 0 | 0.415 5 | -0.002 5 | -0.002 5 | 0.006 5 | 0.161 6 | -0.007 3 | 0.195 5 | ||

| 4 | 0.242 4 | 0.163 2 | 0.384 3 | 0.362 0 | 0.382 7 | 0.395 6 | 0.096 2 | -0.008 6 | 0.136 2 | 0.054 4 | 0.092 3 | 0.078 6 | ||

| 5 | 0.251 3 | 0.259 1 | 0.341 4 | 0.358 5 | 0.277 6 | 0.388 1 | -0.007 0 | -0.007 0 | 0.030 3 | 0.013 8 | 0.124 9 | 0.004 8 | ||

| Ave | 0.231 5 | 0.191 7 | 0.326 7 | 0.367 4 | 0.345 1 | 0.394 4 | 0.015 7 | -0.005 3 | 0.049 7 | 0.066 3 | 0.024 7 | 0.125 7 | ||

| Std | 0.040 2 | 0.047 3 | 0.017 9 | 0.039 1 | 0.024 4 | 0.008 9 | -0.005 2 | -0.005 2 | 0.066 9 | 0.060 3 | -0.045 3 | 0.057 2 | ||

Tab. 2 F1-score and Sharpe ratio comparison on 5 phase data of CSI-300 dataset

| 数据段 | F1分数 | 夏普比率 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ARIMA | MLP | CNN | LSTM | GCN-LSTM | ALSTM | DMMN | ARIMA | MLP | CNN | LSTM | GCN-LSTM | ALSTM | DMMN | |

| 1 | 0.230 3 | 0.166 3 | 0.343 8 | 0.343 2 | 0.353 9 | 0.392 2 | -0.005 2 | -0.005 2 | 0.066 9 | 0.060 3 | -0.045 3 | 0.057 2 | ||

| 2 | 0.213 8 | 0.171 6 | 0.284 8 | 0.365 6 | 0.346 3 | 0.409 2 | -0.003 0 | -0.003 0 | 0.008 8 | 0.041 2 | -0.049 2 | 0.172 1 | ||

| 3 | 0.219 5 | 0.198 4 | 0.274 3 | 0.385 6 | 0.364 0 | 0.415 5 | -0.002 5 | -0.002 5 | 0.006 5 | 0.161 6 | -0.007 3 | 0.195 5 | ||

| 4 | 0.242 4 | 0.163 2 | 0.384 3 | 0.362 0 | 0.382 7 | 0.395 6 | 0.096 2 | -0.008 6 | 0.136 2 | 0.054 4 | 0.092 3 | 0.078 6 | ||

| 5 | 0.251 3 | 0.259 1 | 0.341 4 | 0.358 5 | 0.277 6 | 0.388 1 | -0.007 0 | -0.007 0 | 0.030 3 | 0.013 8 | 0.124 9 | 0.004 8 | ||

| Ave | 0.231 5 | 0.191 7 | 0.326 7 | 0.367 4 | 0.345 1 | 0.394 4 | 0.015 7 | -0.005 3 | 0.049 7 | 0.066 3 | 0.024 7 | 0.125 7 | ||

| Std | 0.040 2 | 0.047 3 | 0.017 9 | 0.039 1 | 0.024 4 | 0.008 9 | -0.005 2 | -0.005 2 | 0.066 9 | 0.060 3 | -0.045 3 | 0.057 2 | ||

| 数据段 | MacroN | MMN | DMMN |

|---|---|---|---|

| 1 | 0.354 3 | 0.362 3 | 0.392 2 |

| 2 | 0.373 1 | 0.373 2 | 0.409 2 |

| 3 | 0.385 8 | 0.399 5 | |

| 4 | 0.405 4 | 0.395 6 | |

| 5 | 0.370 0 | 0.362 5 | 0.388 1 |

| Ave | 0.377 7 | 0.380 0 | 0.394 4 |

| Std | 0.019 1 | 0.019 7 | 0.008 9 |

Tab. 3 Results of ablation experiment

| 数据段 | MacroN | MMN | DMMN |

|---|---|---|---|

| 1 | 0.354 3 | 0.362 3 | 0.392 2 |

| 2 | 0.373 1 | 0.373 2 | 0.409 2 |

| 3 | 0.385 8 | 0.399 5 | |

| 4 | 0.405 4 | 0.395 6 | |

| 5 | 0.370 0 | 0.362 5 | 0.388 1 |

| Ave | 0.377 7 | 0.380 0 | 0.394 4 |

| Std | 0.019 1 | 0.019 7 | 0.008 9 |

| 1 | 扈香梅. 浅谈基本面分析和技术分析在股票市场的应用[J]. 新西部(理论版), 2014(8): 62-62, 64. 10.3969/j.issn.1009-8607(z).2014.03.045 |

| HU X M. The application of fundamental analysis and technical analysis in the stock market[J]. New West, 2014(8):62-62, 64. 10.3969/j.issn.1009-8607(z).2014.03.045 | |

| 2 | 吴玉霞,温欣. 基于ARIMA模型的短期股票价格预测[J]. 统计与决策, 2016(23): 83-86. 10.13546/j.cnki.tjyjc.2016.23.021 |

| WU Y X, WEN X. Short-term stock price forecast based on ARIMA model[J]. Statistics and Decision, 2016(23): 83-86. 10.13546/j.cnki.tjyjc.2016.23.021 | |

| 3 | 陈守东,俞世典. 基于GARCH模型的VaR方法对中国股市的分析[J]. 吉林大学社会科学学报, 2002(4): 11-17. |

| CHEN S D, YU S D. Analysis of China's stock market using VaR method based on GARCH model[J]. Jilin University Journal Social Sciences Edition, 2002(4): 11-17. | |

| 4 | HOU K W. Industry information diffusion and the lead-lag effect in stock returns[J]. The Review of Financial Studies, 2007, 20(4): 1113-1138. 10.1093/revfin/hhm003 |

| 5 | CHAN W S. Stock price reaction to news and no-news: drift and reversal after headlines[J]. Journal of Financial Economics, 2003, 70(2): 223-260. 10.1016/s0304-405x(03)00146-6 |

| 6 | 孙华妤,马跃. 中国货币政策与股票市场的关系[J]. 经济研究, 2003(7): 44-53, 91. |

| SUN H S, MA Y. Monetary policy and stock market in China[J]. Economic Research Journal, 2003(7): 44-53, 91. | |

| 7 | WANG G F, CAO L B, ZHAO H K, et al. Coupling macro-sector-micro financial indicators for learning stock representations with less uncertainty[C]// Proceedings of the 35th AAAI Conference on Artificial Intelligence. Palo Alto, CA: AAAI Press, 2021: 4418-4426. 10.1609/aaai.v35i5.16568 |

| 8 | DIEBOLD F X, YILMAZ K. On the network topology of variance decompositions: measuring the connectedness of financial firms[J]. Journal of Econometrics, 2014, 182(1): 119-134. 10.1016/j.jeconom.2014.04.012 |

| 9 | NOH J D. Model for correlations in stock markets[J]. Physical Review. E, Statistical Physics, Plasmas, Fluids, and Related Interdisciplinary Topics, 2000, 61(5): 5981-5982. 10.1103/physreve.61.5981 |

| 10 | 刘文杰. 新冠肺炎疫情对互联网视频行业的影响[J]. 人文天下, 2020(10): 10-14. 10.3969/j.issn.2095-3690.2020.10.003 |

| LIU W J. The impact of the COVID-19 on the Internet video industry[J]. Humanities in the World, 2020(10): 10-14. 10.3969/j.issn.2095-3690.2020.10.003 | |

| 11 | 夏杰长,丰晓旭. 新冠肺炎疫情对旅游业的冲击与对策[J]. 中国流通经济, 2020, 34(3): 3-10. 10.14100/j.cnki.65-1039/g4.20200812.001 |

| XIA J C, FENG X X. The impact of the novel coronavirus outbreak on the tourism industry and its countermeasures[J]. China Business and Market, 2020, 34(3): 3-10. 10.14100/j.cnki.65-1039/g4.20200812.001 | |

| 12 | XU Y M, COHEN S B. Stock movement prediction from tweets and historical prices[C]// Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). Stroudsburg, PA: ACL, 2018: 1970-1979. 10.18653/v1/p18-1183 |

| 13 | FENG F L, CHEN H M, HE X N, et al. Enhancing stock movement prediction with adversarial training[C]// Proceedings of the 28th International Joint Conference on Artificial Intelligence. California: ijcai.org, 2019: 5843-5849. 10.24963/ijcai.2019/810 |

| 14 | DING Q G, WU S F, SUN H, et al. Hierarchical multi-scale Gaussian transformer for stock movement prediction[C]// Proceedings of the 29th International Joint Conference on Artificial Intelligence. California: ijcai.org, 2020: 4640-4646. 10.24963/ijcai.2020/640 |

| 15 | YE J X, ZHAO J J, YE K J, et al. Multi-graph convolutional network for relationship-driven stock movement prediction[C]// Proceedings of the 25th International Conference on Pattern Recognition. Piscataway: IEEE, 2021: 6702-6709. 10.1109/icpr48806.2021.9412695 |

| 16 | SAWHNEY R, AGARWAL S, WADHWA A, et al. Spatiotemporal hypergraph convolution network for stock movement forecasting[C]// Proceedings of the 2020 IEEE International Conference on Data Mining. Piscataway: IEEE, 2020: 482-491. 10.1109/icdm50108.2020.00057 |

| 17 | KODOGIANNIS V, LOLIS A. Forecasting financial time series using neural network and fuzzy system-based techniques[J]. Neural Computing and Applications, 2002, 11(2): 90-102. 10.1007/s005210200021 |

| 18 | JIANG W W. Applications of deep learning in stock market prediction: recent progress[J]. Expert Systems with Applications, 2021, 184: No.115537. 10.1016/j.eswa.2021.115537 |

| 19 | HUYNH H D, DANG L M, DUONG D. A new model for stock price movements prediction using deep neural network[C]// Proceedings of the 8th International Symposium on Information and Communication Technology. New York: ACM, 2017: 57-62. 10.1145/3155133.3155202 |

| 20 | NELSON D M Q, PEREIRA A C M, DE OLIVEIRA R A. Stock market's price movement prediction with LSTM neural networks[C]// Proceedings of the 2017 International Joint Conference on Neural Networks. Piscataway: IEEE, 2017: 1419-1426. 10.1109/ijcnn.2017.7966019 |

| 21 | 邓凤欣,王洪良. LSTM神经网络在股票价格趋势预测中的应用——基于美港股票市场个股数据的研究[J]. 金融经济, 2018(14): 96-98. |

| DENG F X, WANG H L. The application of LSTM neural network in stock price trend prediction - based on the research of individual stock data in the US and Hong Kong stock markets[J]. Finance Economy, 2018(14):96-98. | |

| 22 | HOCHREITER S, SCHMIDHUBER J. Long short-term memory[J]. Neural Computation, 1997, 9(8): 1735-1780. 10.1162/neco.1997.9.8.1735 |

| 23 | LI W, BAO R H, HARIMOTO K, et al. Modeling the stock relation with graph network for overnight stock movement prediction[C]// Proceedings of the 29th International Joint Conference on Artificial Intelligence. California: ijcai.org, 2020: 4541-4547. 10.24963/ijcai.2020/626 |

| 24 | 饶东宁,邓福栋,蒋志华. 基于多信息源的股价趋势预测[J]. 计算机科学, 2017, 44(10): 193-202. 10.11896/j.issn.1002-137X.2017.10.036 |

| RAO D N, DENG F D, JIANG Z H. Stock price movement prediction based on multisources[J]. Computer Science, 2017, 44(10): 193-202. 10.11896/j.issn.1002-137X.2017.10.036 | |

| 25 | 张梦吉,杜婉钰,郑楠. 引入新闻短文本的个股走势预测模型[J]. 数据分析与知识发现, 2019, 3(5): 11-18. 10.11925/infotech.2096-3467.2018.0871 |

| ZHANG M J, DU W Y, ZHENG N. Predicting stock trends based on news events[J]. Data Analysis and Knowledge Discovery, 2019, 3(5): 11-18. 10.11925/infotech.2096-3467.2018.0871 | |

| 26 | KRYSOVATYY A, VASYLCHYSHYN O, DESYATNYUK O, et al. News feed for stock movement prediction[C]// Proceedings of the 15th International Conference on ICT in Education, Research and Industrial Applications, Volume I: Main Conference. Aachen: CEUR-WS.org, 2019: 90-97. |

| 27 | 杨丽,吴雨茜,王俊丽,等. 循环神经网络研究综述[J]. 计算机应用, 2018, 38(S2): 1-6, 26. |

| YANG L, WU Y X, WANG J L, et al. Research on recurrent neural network[J]. Journal of Computer Applications, 2018, 38(S2): 1-6, 26. | |

| 28 | CHO K, van MERRIËNBOER B, GU̇LÇEHRE Ç, et al. Learning phrase representations using RNN encoder-decoder for statistical machine translation[C]// Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing. Stroudsburg, PA: ACL, 2014: 1724-1734. 10.3115/v1/d14-1179 |

| [1] | Zhirong HOU, Xiaodong FAN, Hua ZHANG, Xiaonan MA. J-SGPGN: paraphrase generation network based on joint learning of sequence and graph [J]. Journal of Computer Applications, 2023, 43(5): 1365-1371. |

| [2] | Yu TAN, Xiaoqin WANG, Rushi LAN, Zhenbing LIU, Xiaonan LUO. Multi-label cross-modal hashing retrieval based on discriminative matrix factorization [J]. Journal of Computer Applications, 2023, 43(5): 1349-1354. |

| [3] | Xinwei LYU, Shuxia LU. Iteratively modified robust extreme learning machine [J]. Journal of Computer Applications, 2023, 43(5): 1342-1348. |

| [4] |

.

Multiple clustering algorithm based on dynamic weighted tensor distance#br#

#br#

#br#

[J]. Journal of Computer Applications, 0, (): 0-0.

|

| [5] | . Spectral clustering based dynamic community discovery algorithm in social network [J]. Journal of Computer Applications, 0, (): 0-0. |

| [6] |

.

Collaborative filtering algorithm based on collaborative training and Boosting#br#

#br#

[J]. Journal of Computer Applications, 0, (): 0-0.

|

| [7] | Yinjiang CAI, Guangjun XU, Xibo MA. Data enhancement method for drugs under graph-structured representation [J]. Journal of Computer Applications, 2023, 43(4): 1136-1141. |

| [8] | Jin XIA, Zhengqun WANG, Shiming ZHU. Traffic flow prediction model based on time series decomposition [J]. Journal of Computer Applications, 2023, 43(4): 1129-1135. |

| [9] | Nanfan LI, Wenwen SI, Siyuan DU, Zhiyong WANG, Chongyang ZHONG, Shihong XIA. Hidden state initialization method for recurrent neural network-based human motion model [J]. Journal of Computer Applications, 2023, 43(3): 723-727. |

| [10] | Mengting WANG, Wenzhong YANG, Yongzhi WU. Survey of single target tracking algorithms based on Siamese network [J]. Journal of Computer Applications, 2023, 43(3): 661-673. |

| [11] | Huayong YAO, Dongyi YE, Zhaojiong CHEN. Multi-round conversational reinforcement learning recommendation algorithm via multi-granularity feedback [J]. Journal of Computer Applications, 2023, 43(1): 15-21. |

| [12] | Sai ZHENG, Tianrui LI, Wei HUANG. Federated learning algorithm for communication cost optimization [J]. Journal of Computer Applications, 2023, 43(1): 1-7. |

| [13] | Yu LU, Lingyun ZHAO, Binwen BAI, Zhen JIANG. Imbalanced classification algorithm based on improved semi-supervised clustering [J]. Journal of Computer Applications, 2022, 42(12): 3750-3755. |

| [14] | Tiankai LIANG, Bi ZENG, Guang CHEN. Federated learning survey:concepts, technologies, applications and challenges [J]. Journal of Computer Applications, 2022, 42(12): 3651-3662. |

| [15] | Lingmin LI, Mengran HOU, Kun CHEN, Junmin LIU. Survey on interpretability research of deep learning [J]. Journal of Computer Applications, 2022, 42(12): 3639-3650. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||