Journal of Computer Applications ›› 2022, Vol. 42 ›› Issue (7): 2265-2273.DOI: 10.11772/j.issn.1001-9081.2021081487

• Frontier and comprehensive applications • Previous Articles Next Articles

Xiaohan LI1( ), Jun WANG1, Huading JIA1, Liu XIAO2

), Jun WANG1, Huading JIA1, Liu XIAO2

Received:2021-08-19

Revised:2021-11-30

Accepted:2021-12-03

Online:2022-01-07

Published:2022-07-10

Contact:

Xiaohan LI

About author:WANG Jun, born in 1987, Ph. D., associate professor. His research interests include financial technology, financial intelligence.Supported by:

李晓寒1(), 王俊1, 贾华丁1, 萧刘2

通讯作者:

李晓寒

作者简介:王俊(1987—),男,山东青岛人,副教授,博士,CCF会员,主要研究方向:金融科技、金融智能基金资助:CLC Number:

Xiaohan LI, Jun WANG, Huading JIA, Liu XIAO. Stock market volatility prediction method based on graph neural network with multi-attention mechanism[J]. Journal of Computer Applications, 2022, 42(7): 2265-2273.

李晓寒, 王俊, 贾华丁, 萧刘. 基于多重注意力机制的图神经网络股市波动预测方法[J]. 《计算机应用》唯一官方网站, 2022, 42(7): 2265-2273.

Add to citation manager EndNote|Ris|BibTeX

URL: https://www.joca.cn/EN/10.11772/j.issn.1001-9081.2021081487

Fig.1 Overall framework of the proposed model

Fig.2 Graph data embedding method

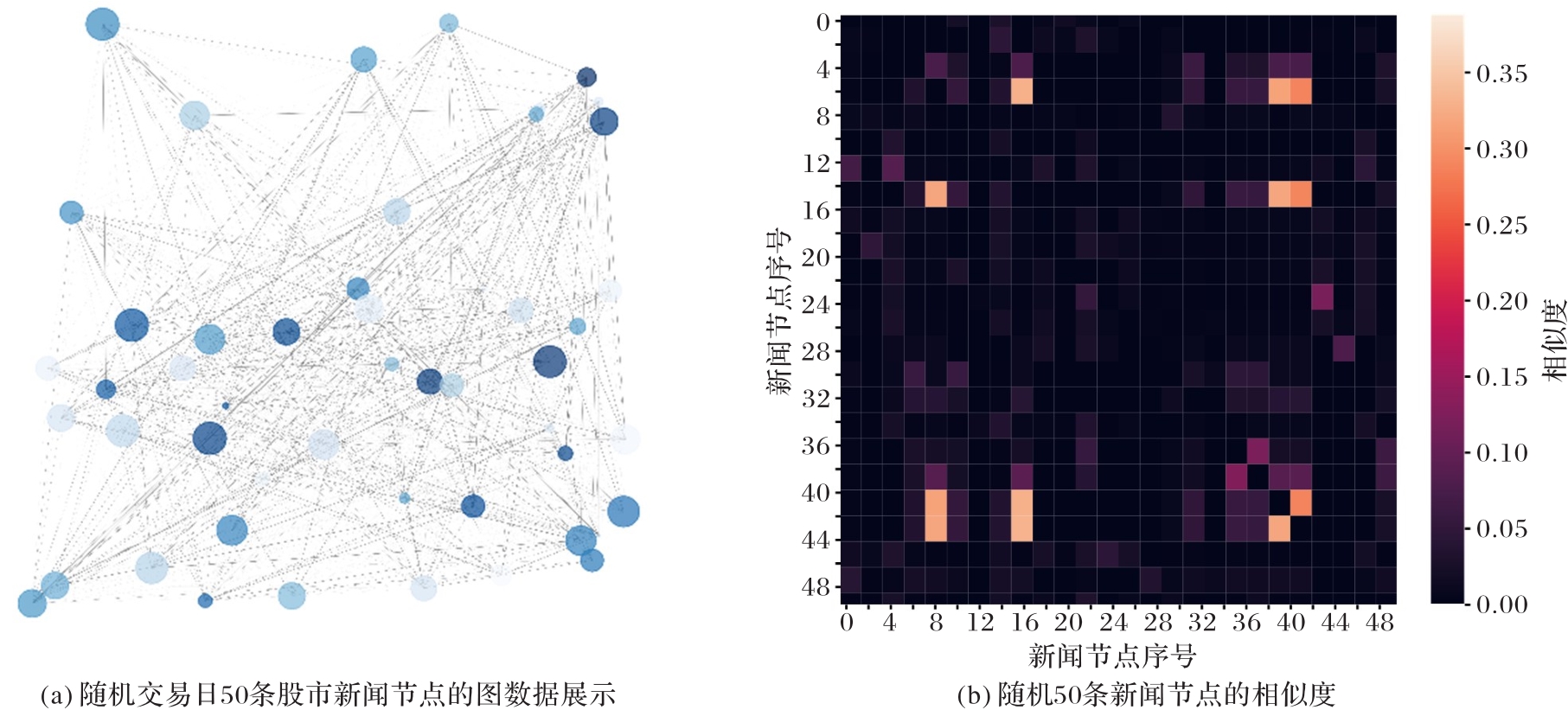

Fig.3 Stock market news graph data

Fig.4 Training process of graph neural network

| 方法 | 卷积名称 | Input size | Out size | Drop Rate | Aggregator Type |

|---|---|---|---|---|---|

| 本文方法 | GRATConv1 | 200 | 128 | 0.1 | LSTM |

| GRATConv2 | 128 | 64 | 0.0 | LSTM | |

| GAT | GATConv1 | 200 | 128 | 0.1 | num_heads=3 |

| GATConv2 | 128 | 64 | 0.0 | num_heads=3 | |

| RelGraph | RelGraphConv1 | 200 | 128 | 0.1 | regularizer=basis |

| RelGraphConv2 | 128 | 64 | 0.0 | regularizer=basis | |

| Edge | EdgeConv1 | 200 | 128 | 0.1 | |

| EdgeConv2 | 128 | 64 | 0.0 | ||

| SAGE | SAGEConv1 | 200 | 128 | 0.1 | LSTM |

| SAGEConv2 | 128 | 64 | 0.0 | LSTM |

Tab. 2 Parameter setting of experimental networks

| 方法 | 卷积名称 | Input size | Out size | Drop Rate | Aggregator Type |

|---|---|---|---|---|---|

| 本文方法 | GRATConv1 | 200 | 128 | 0.1 | LSTM |

| GRATConv2 | 128 | 64 | 0.0 | LSTM | |

| GAT | GATConv1 | 200 | 128 | 0.1 | num_heads=3 |

| GATConv2 | 128 | 64 | 0.0 | num_heads=3 | |

| RelGraph | RelGraphConv1 | 200 | 128 | 0.1 | regularizer=basis |

| RelGraphConv2 | 128 | 64 | 0.0 | regularizer=basis | |

| Edge | EdgeConv1 | 200 | 128 | 0.1 | |

| EdgeConv2 | 128 | 64 | 0.0 | ||

| SAGE | SAGEConv1 | 200 | 128 | 0.1 | LSTM |

| SAGEConv2 | 128 | 64 | 0.0 | LSTM |

| 方法 | 参数 |

|---|---|

| SVM | C=0.8;kernel=liner;max_iter=1 000 |

| RF | Max_ feature=none;min_samples_split=10;n_estimators=3 |

| MKKM | View=3;kernel=RBF;gamma=1/3;k=2 |

| TeSIA | Tensor_order=3;tensor_size(i=5, j=1,k=10);Max_iter=5 000 |

Tab. 3 Parameter setting of experimental models

| 方法 | 参数 |

|---|---|

| SVM | C=0.8;kernel=liner;max_iter=1 000 |

| RF | Max_ feature=none;min_samples_split=10;n_estimators=3 |

| MKKM | View=3;kernel=RBF;gamma=1/3;k=2 |

| TeSIA | Tensor_order=3;tensor_size(i=5, j=1,k=10);Max_iter=5 000 |

| 方法 | 上证综合指数 | 沪深300指数 | 深证成份指数 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 交易日T+1 | 交易日T+2 | 交易日T+3 | 交易日T+1 | 交易日T+2 | 交易日T+3 | 交易日T+1 | 交易日T+2 | 交易日T+3 | ||||||||||

| 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | |

| 本文方法 | 0.65 | 0.58 | 0.75 | 0.73 | 0.61 | 0.60 | 0.75 | 0.76 | 0.90 | 0.85 | 0.72 | 0.63 | 0.65 | 0.64 | 0.89 | 0.91 | 0.66 | 0.73 |

| GATConv | 0.53 | 0.58 | 0.57 | 0.51 | 0.46 | 0.43 | 0.69 | 0.53 | 0.49 | 0.45 | 0.62 | 0.47 | 0.48 | 0.52 | 0.63 | 0.61 | 0.42 | 0.45 |

| RelGraphConv | 0.52 | 0.53 | 0.49 | 0.50 | 0.47 | 0.39 | 0.64 | 0.54 | 0.63 | 0.49 | 0.55 | 0.47 | 0.44 | 0.47 | 0.45 | 0.53 | 0.47 | 0.50 |

| EdgeConv | 0.39 | 0.37 | 0.61 | 0.56 | 0.31 | 0.38 | 0.50 | 0.51 | 0.54 | 0.53 | 0.59 | 0.53 | 0.47 | 0.45 | 0.34 | 0.44 | 0.38 | 0.41 |

| SAGEConv | 0.48 | 0.45 | 0.50 | 0.48 | 0.52 | 0.49 | 0.43 | 0.38 | 0.39 | 0.49 | 0.52 | 0.38 | 0.38 | 0.47 | 0.30 | 0.38 | 0.31 | 0.33 |

| SVM | 0.58 | 0.56 | 0.58 | 0.55 | 0.54 | 0.53 | 0.46 | 0.46 | 0.47 | 0.48 | 0.46 | 0.45 | 0.44 | 0.47 | 0.57 | 0.58 | 0.43 | 0.40 |

| RF | 0.56 | 0.60 | 0.60 | 0.59 | 0.55 | 0.52 | 0.56 | 0.55 | 0.51 | 0.53 | 0.51 | 0.48 | 0.57 | 0.52 | 0.52 | 0.43 | 0.53 | 0.46 |

| MKKM | 0.58 | 0.56 | 0.62 | 0.60 | 0.60 | 0.59 | 0.68 | 0.66 | 0.68 | 0.70 | 0.62 | 0.57 | 0.62 | 0.56 | 0.63 | 0.70 | 0.65 | 0.58 |

| TeSIA | 0.52 | 0.58 | 0.63 | 0.62 | 0.58 | 0.57 | 0.62 | 0.67 | 0.69 | 0.73 | 0.68 | 0.56 | 0.61 | 0.59 | 0.63 | 0.57 | 0.62 | 0.59 |

Tab. 4 Predicted results comparison of different indexes

| 方法 | 上证综合指数 | 沪深300指数 | 深证成份指数 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 交易日T+1 | 交易日T+2 | 交易日T+3 | 交易日T+1 | 交易日T+2 | 交易日T+3 | 交易日T+1 | 交易日T+2 | 交易日T+3 | ||||||||||

| 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | 召回率 | 准确率 | |

| 本文方法 | 0.65 | 0.58 | 0.75 | 0.73 | 0.61 | 0.60 | 0.75 | 0.76 | 0.90 | 0.85 | 0.72 | 0.63 | 0.65 | 0.64 | 0.89 | 0.91 | 0.66 | 0.73 |

| GATConv | 0.53 | 0.58 | 0.57 | 0.51 | 0.46 | 0.43 | 0.69 | 0.53 | 0.49 | 0.45 | 0.62 | 0.47 | 0.48 | 0.52 | 0.63 | 0.61 | 0.42 | 0.45 |

| RelGraphConv | 0.52 | 0.53 | 0.49 | 0.50 | 0.47 | 0.39 | 0.64 | 0.54 | 0.63 | 0.49 | 0.55 | 0.47 | 0.44 | 0.47 | 0.45 | 0.53 | 0.47 | 0.50 |

| EdgeConv | 0.39 | 0.37 | 0.61 | 0.56 | 0.31 | 0.38 | 0.50 | 0.51 | 0.54 | 0.53 | 0.59 | 0.53 | 0.47 | 0.45 | 0.34 | 0.44 | 0.38 | 0.41 |

| SAGEConv | 0.48 | 0.45 | 0.50 | 0.48 | 0.52 | 0.49 | 0.43 | 0.38 | 0.39 | 0.49 | 0.52 | 0.38 | 0.38 | 0.47 | 0.30 | 0.38 | 0.31 | 0.33 |

| SVM | 0.58 | 0.56 | 0.58 | 0.55 | 0.54 | 0.53 | 0.46 | 0.46 | 0.47 | 0.48 | 0.46 | 0.45 | 0.44 | 0.47 | 0.57 | 0.58 | 0.43 | 0.40 |

| RF | 0.56 | 0.60 | 0.60 | 0.59 | 0.55 | 0.52 | 0.56 | 0.55 | 0.51 | 0.53 | 0.51 | 0.48 | 0.57 | 0.52 | 0.52 | 0.43 | 0.53 | 0.46 |

| MKKM | 0.58 | 0.56 | 0.62 | 0.60 | 0.60 | 0.59 | 0.68 | 0.66 | 0.68 | 0.70 | 0.62 | 0.57 | 0.62 | 0.56 | 0.63 | 0.70 | 0.65 | 0.58 |

| TeSIA | 0.52 | 0.58 | 0.63 | 0.62 | 0.58 | 0.57 | 0.62 | 0.67 | 0.69 | 0.73 | 0.68 | 0.56 | 0.61 | 0.59 | 0.63 | 0.57 | 0.62 | 0.59 |

Fig.5 Prediction ROC AUC diagrams of different classifiers

Fig.6 Strategy returns of different indexes

| 1 | FAMA E F. Efficient capital markets: a review of theory and empirical work[J]. The Journal of Finance, 1970, 25(2): 383-417. 10.1111/j.1540-6261.1970.tb00518.x |

| 2 | KAHNEMAN D. Maps of bounded rationality: psychology for behavioral economics[J]. The American Economic Review, 2003, 93(5): 1449-1475. 10.1257/000282803322655392 |

| 3 | SHILLER R J. Irrational Exuberance[M]. Revised and Expanded 3rd Ed. Princeton: Princeton University Press, 2016:237-267. 10.1515/9781400865536 |

| 4 | HONG H, KUBIK J D, STEIN J C. Social interaction and stock-market participation[J]. The Journal of Finance, 2004, 59(1): 137-163. 10.1111/j.1540-6261.2004.00629.x |

| 5 | STROHSAL T, WEBER E. Time-varying international stock market interaction and the identification of volatility signals[J]. Journal of Banking and Finance, 2015, 56: 28-36. 10.1016/j.jbankfin.2015.01.020 |

| 6 | OLIVEIRA N, CORTEZ P, AREAL N. The impact of microblogging data for stock market prediction: using Twitter to predict returns, volatility, trading volume and survey sentiment indices[J]. Expert Systems with Applications, 2017, 73: 125-144. 10.1016/j.eswa.2016.12.036 |

| 7 | CAKICI N, FABOZZI F J, TAN S. Size, value, and momentum in emerging market stock returns[J]. Emerging Markets Review, 2013, 16: 46-65. 10.1016/j.ememar.2013.03.001 |

| 8 | BURTON R F. Why is the body mass index calculated as mass/height2, not as mass/height3?[J]. Annals of Human Biology, 2007, 34(6): 656-663. 10.1080/03014460701732962 |

| 9 | TETLOCK P C. Giving content to investor sentiment: the role of media in the stock market[J]. The Journal of Finance, 2007, 62(3): 1139-1168. 10.1111/j.1540-6261.2007.01232.x |

| 10 | BARBER B M, ODEAN T. All that glitters: the effect of attention and news on the buying behavior of individual and institutional investors[J]. The Review of Financial Studies, 2008, 21(2): 785-818. 10.1093/rfs/hhm079 |

| 11 | ATKINS A, NIRANJAN M, GERDING E. Financial news predicts stock market volatility better than close price[J]. The Journal of Finance and Data Science, 2018, 4(2): 120-137. 10.1016/j.jfds.2018.02.002 |

| 12 | WEI Y C, LU Y C, CHEN J N, et al. Informativeness of the market news sentiment in the Taiwan stock market[J]. The North American Journal of Economics and Finance, 2017, 39: 158-181. 10.1016/j.najef.2016.10.004 |

| 13 | SIMON H A. Designing organizations for an information-rich world[J]. International Library of Critical Writings in Economics, 1996, 70: 187-202. |

| 14 | CHAN W S. Stock price reaction to news and no-news: drift and reversal after headlines[J]. Journal of Financial Economics, 2003, 70(2): 223-260. 10.1016/s0304-405x(03)00146-6 |

| 15 | 王晓丹,尚维,汪寿阳. 互联网新闻媒体报道对我国股市的影响分析[J]. 系统工程理论与实践, 2019, 39(12):3038-3047. 10.12011/1000-6788-2017-0445-10 |

| WANG X D, SHANG W, WANG S Y. The effects of online news on the Chinese stock market[J]. System Engineering — Theory and Practice, 2019, 39(12):3038-3047. 10.12011/1000-6788-2017-0445-10 | |

| 16 | LIU J, LU Z C, DU W. Combining enterprise knowledge graph and news sentiment analysis for stock price prediction[C/OL]// Proceedings of the 52nd Hawaii International Conference on System Sciences. [2021-07-02].. 10.24251/hicss.2019.153 |

| 17 | THAKKAR A, CHAUDHARI K. Fusion in stock market prediction: a decade survey on the necessity, recent developments, and potential future directions[J]. Information Fusion, 2021, 65: 95-107. 10.1016/j.inffus.2020.08.019 |

| 18 | ZHANG X, ZHANG Y J, WANG S Z, et al. Improving stock market prediction via heterogeneous information fusion[J]. Knowledge-Based Systems, 2018, 143: 236-247. 10.1016/j.knosys.2017.12.025 |

| 19 | KIM T, KIM H Y. Forecasting stock prices with a feature fusion LSTM-CNN model using different representations of the same data[J]. PLoS ONE, 2019, 14(2): No.e0212320. 10.1371/journal.pone.0212320 |

| 20 | HASSAN M R, NATH B, KIRLEY M. A fusion model of HMM, ANN and GA for stock market forecasting[J]. Expert Systems with Applications, 2007, 33(1): 171-180. 10.1016/j.eswa.2006.04.007 |

| 21 | ZHANG Q, YANG L J, ZHOU F. Attention enhanced long short-term memory network with multi-source heterogeneous information fusion: an application to BGI Genomics[J]. Information Sciences, 2021, 553: 305-330. 10.1016/j.ins.2020.10.023 |

| 22 | PATEL J, SHAH S, THAKKAR P, et al. Predicting stock market index using fusion of machine learning techniques[J]. Expert Systems with Applications, 2015, 42(4): 2162-2172. 10.1016/j.eswa.2014.10.031 |

| 23 | 李晓寒,贾华丁,程雪,等. 基于改进遗传算法和图神经网络的股市波动预测方法[J/OL]. 计算机应用. (2021-08-17) [2021-08-20].. |

| LI X H, JIA H D, CHENG X, et al. Stock market fluctuation prediction method based on improved genetic algorithm and graph neural network[J/OL]. Journal of Computer Applications. (2021-08-17) [2021-08-20].. | |

| 24 | KAHNEMAN D, TVERSKY A. On the interpretation of intuitive probability: a reply to Jonathan Cohen[J]. Cognition, 1979, 7(4): 409-411. 10.1016/0010-0277(79)90024-6 |

| 25 | LO A W, MacKINLAY A C. Stock market prices do not follow random walks: evidence from a simple specification test[J]. The Review of Financial Studies, 1988, 1(1): 41-66. 10.1093/rfs/1.1.41 |

| 26 | TANG H, CHIU K C, XU L. Finite mixture of ARMA-GARCH model for stock price prediction[C/OL]// Proceedings of the 3rd International Workshop on Computational Intelligence in Economics and Finance. [2018-10-10].. |

| 27 | ROJAS I, VALENZUELA O, ROJAS F, et al. Soft-computing techniques and ARMA model for time series prediction[J]. Neurocomputing, 2008, 71(4/5/6): 519-537. 10.1016/j.neucom.2007.07.018 |

| 28 | JEGADEESH N, TITMAN S. Returns to buying winners and selling losers: implications for stock market efficiency[J]. The Journal of Finance, 1993, 48(1): 65-91. 10.1111/j.1540-6261.1993.tb04702.x |

| 29 | FAMA E F, FRENCH K R. The cross-section of expected stock returns[J]. The Journal of Finance, 1992, 47(2):427-465. 10.1111/j.1540-6261.1992.tb04398.x |

| 30 | FAMA E F, FRENCH F K R. Multifactor explanations of asset pricing anomalies[J]. The Journal of Finance, 1996, 51(1):55-84. 10.1111/j.1540-6261.1996.tb05202.x |

| 31 | SI J F, MUKHERJEE A, LIU B, et al. Exploiting topic based twitter sentiment for stock prediction[C]// Proceedings of the 51st Annual Meeting of the Association for Computational Linguistics (Volume 2: Short Papers). Stroudsburg, PA: Association for Computational Linguistics, 2013: 24-29. |

| 32 | DING X, ZHANG Y, LIU T, et al. Deep learning for event-driven stock prediction[C]// Proceedings of the 24th International Joint Conference on Artificial Intelligence. Palo Alto, CA: AAAI Press, 2015: 2327-2333. |

| 33 | DING X, ZHANG Y, LIU T, et al. Using structured events to predict stock price movement: an empirical investigation[C]// Proceedings of the Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing. Stroudsburg, PA: Association for Computational Linguistics, 2014: 1415-1425. 10.3115/v1/d14-1148 |

| 34 | TAN J H, WANG J, RINPRASERTMEECHAI D, et al. A tensor-based eLSTM model to predict stock price using financial news[C/OL]// Proceedings of the 52nd Hawaii International Conference on System Sciences. [2021-07-02].. 10.24251/hicss.2019.201 |

| 35 | CHAI L, XU H F, LUO Z M, et al. A multi-source heterogeneous data analytic method for future price fluctuation prediction[J]. Neurocomputing, 2020, 418: 11-20. 10.1016/j.neucom.2020.07.073 |

| 36 | ZHANG X, LI Y X, WANG S Z, et al. Enhancing stock market prediction with extended coupled hidden Markov model over multi-sourced data[J]. Knowledge and Information Systems, 2019, 61(2): 1071-1090. 10.1007/s10115-018-1315-6 |

| 37 | KIM R, SO C H, JEONG M, et al. HATS: a hierarchical graph attention network for stock movement prediction[EB/OL]. (2019-11-12) [2021-06-20].. |

| 38 | LI Q, WANG J, WANG F, et al. The role of social sentiment in stock markets: a view from joint effects of multiple information sources[J]. Multimedia Tools and Applications, 2017, 76(10): 12315-12345. 10.1007/s11042-016-3643-4 |

| 39 | 呼延康,樊鑫,余乐天,等. 图神经网络回归的人脸超分辨率重建[J]. 软件学报, 2018, 29(4):914-925. |

| HUYAN K, FAN X, YU L T, et al. Graph based neural network regression strategy for facial image super-resolution[J]. Journal of Software, 2018, 29(4):914-925. | |

| 40 | KIM K-J, HAN I. Genetic algorithms approach to feature discretization in artificial neural networks for the prediction of stock price index[J]. Expert Systems with Applications, 2000, 19(2): 125-132. 10.1016/s0957-4174(00)00027-0 |

| 41 | LI Q, JIANG L L, LI P, et al. Tensor-based learning for predicting stock movements[C]// Proceedings of 29th AAAI Conference on Artificial Intelligence. Palo Alto, CA: AAAI Press, 2015:1784-1790. 10.1609/aaai.v29i1.9452 |

| 42 | BRUNA J, ZAREMBA W, SZLAM A, et al. Spectral networks and locally connected networks on graphs[EB/OL]. (2014-05-21) [2021-06-20].. |

| 43 | DEFFERRARD M, BRESSON X, VANDERGHEYNST P. Convolutional neural networks on graphs with fast localized spectral filtering[C]// Proceedings of the 30th International Conference on Neural Information Processing Systems. Red Hook, NY: Curran Associates Inc., 2016: 3844-3852. |

| 44 | KIPF T N, WELLING M. Semi-supervised classification with graph convolutional networks[EB/OL]. (2017-02-22) [2021-06-20].. |

| 45 | LIU Y, ZENG Q G, YANG H R, et al. Stock price movement prediction from financial news with deep learning and knowledge graph embedding[C]// Proceedings of the 2018 Pacific Rim Knowledge Acquisition Workshop, LNCS 11016. Cham: Springer, 2018: 102-113. |

| 46 | MATSUNAGA D, SUZUMURA T, TAKAHASHI T. Exploring graph neural networks for stock market predictions with rolling window analysis[EB/OL]. (2019-11-27) [2021-06-20].. |

| 47 | HUANG T L. The puzzling media effect in the Chinese stock market[J]. Pacific-Basin Finance Journal, 2018, 49: 129-146. 10.1016/j.pacfin.2018.04.005 |

| 48 | ARASU A, WIDOM J. Resource sharing in continuous sliding-window aggregates[C]// Proceedings of the 30th International Conference on Very Large Data Bases. [S.l.]: VLDB Endowment, 2004: 336-347. 10.1016/b978-012088469-8.50032-2 |

| [1] | Xingyao YANG, Yu CHEN, Jiong YU, Zulian ZHANG, Jiaying CHEN, Dongxiao WANG. Recommendation model combining self-features and contrastive learning [J]. Journal of Computer Applications, 2024, 44(9): 2704-2710. |

| [2] | Tingjie TANG, Jiajin HUANG, Jin QIN. Session-based recommendation with graph auxiliary learning [J]. Journal of Computer Applications, 2024, 44(9): 2711-2718. |

| [3] | Hang YANG, Wanggen LI, Gensheng ZHANG, Zhige WANG, Xin KAI. Multi-layer information interactive fusion algorithm based on graph neural network for session-based recommendation [J]. Journal of Computer Applications, 2024, 44(9): 2719-2725. |

| [4] | Yu DU, Yan ZHU. Constructing pre-trained dynamic graph neural network to predict disappearance of academic cooperation behavior [J]. Journal of Computer Applications, 2024, 44(9): 2726-2731. |

| [5] | Ying YANG, Xiaoyan HAO, Dan YU, Yao MA, Yongle CHEN. Graph data generation approach for graph neural network model extraction attacks [J]. Journal of Computer Applications, 2024, 44(8): 2483-2492. |

| [6] | Fan YANG, Yao ZOU, Mingzhi ZHU, Zhenwei MA, Dawei CHENG, Changjun JIANG. Credit card fraud detection model based on graph attention Transformation neural network [J]. Journal of Computer Applications, 2024, 44(8): 2634-2642. |

| [7] | Xinrui LIN, Xiaofei WANG, Yan ZHU. Academic anomaly citation group detection based on local extended community detection [J]. Journal of Computer Applications, 2024, 44(6): 1855-1861. |

| [8] | Yao DONG, Yixue FU, Yongfeng DONG, Jin SHI, Chen CHEN. Survey of incomplete multi-view clustering [J]. Journal of Computer Applications, 2024, 44(6): 1673-1682. |

| [9] | Jiong WANG, Taotao TANG, Caiyan JIA. PAGCL: positive augmentation graph contrastive learning recommendation method without negative sampling [J]. Journal of Computer Applications, 2024, 44(5): 1485-1492. |

| [10] | Jie GUO, Jiayu LIN, Zuhong LIANG, Xiaobo LUO, Haitao SUN. Recommendation method based on knowledge‑awareness and cross-level contrastive learning [J]. Journal of Computer Applications, 2024, 44(4): 1121-1127. |

| [11] | Dapeng XU, Xinmin HOU. Feature selection method for graph neural network based on network architecture design [J]. Journal of Computer Applications, 2024, 44(3): 663-670. |

| [12] | Nengbing HU, Biao CAI, Xu LI, Danhua CAO. Graph classification method based on graph pooling contrast learning [J]. Journal of Computer Applications, 2024, 44(11): 3327-3334. |

| [13] | Beijing ZHOU, Hairong WANG, Yimeng WANG, Lisi ZHANG, He MA. Recommendation method using knowledge graph embedding propagation [J]. Journal of Computer Applications, 2024, 44(10): 3252-3259. |

| [14] | Hongbin WANG, Xiao FANG, Hong JIANG. Commonsense reasoning and question answering method with three-dimensional semantic features [J]. Journal of Computer Applications, 2024, 44(1): 138-144. |

| [15] | Junhao LUO, Yan ZHU. Multi-dynamic aware network for unaligned multimodal language sequence sentiment analysis [J]. Journal of Computer Applications, 2024, 44(1): 79-85. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||