Journal of Computer Applications ›› 2026, Vol. 46 ›› Issue (2): 427-436.DOI: 10.11772/j.issn.1001-9081.2025080955

• Artificial intelligence • Previous Articles

Hanyue WEI, Chenjuan GUO( ), Jieyuan MEI, Jindong TIAN, Peng CHEN, Ronghui XU, Bin YANG

), Jieyuan MEI, Jindong TIAN, Peng CHEN, Ronghui XU, Bin YANG

Received:2025-08-20

Revised:2025-09-11

Accepted:2025-10-10

Online:2026-03-02

Published:2026-02-10

Contact:

Chenjuan GUO

About author:WEI Hanyue, born in 1999, M. S. candidate. Her research interests include financial time series forecasting, multimodal forecasting.Supported by:

魏涵玥, 郭晨娟(), 梅杰源, 田锦东, 陈鹏, 徐榕荟, 杨彬

通讯作者:

郭晨娟

作者简介:魏涵玥(1999—),女,江苏苏州人,硕士研究生,主要研究方向:金融时序预测、多模态预测基金资助:CLC Number:

Hanyue WEI, Chenjuan GUO, Jieyuan MEI, Jindong TIAN, Peng CHEN, Ronghui XU, Bin YANG. MATCH: multimodal stock prediction framework integrating time-frequency features and hybrid text[J]. Journal of Computer Applications, 2026, 46(2): 427-436.

魏涵玥, 郭晨娟, 梅杰源, 田锦东, 陈鹏, 徐榕荟, 杨彬. 融合时频特征与混合文本的多模态股票预测框架MATCH[J]. 《计算机应用》唯一官方网站, 2026, 46(2): 427-436.

Add to citation manager EndNote|Ris|BibTeX

URL: https://www.joca.cn/EN/10.11772/j.issn.1001-9081.2025080955

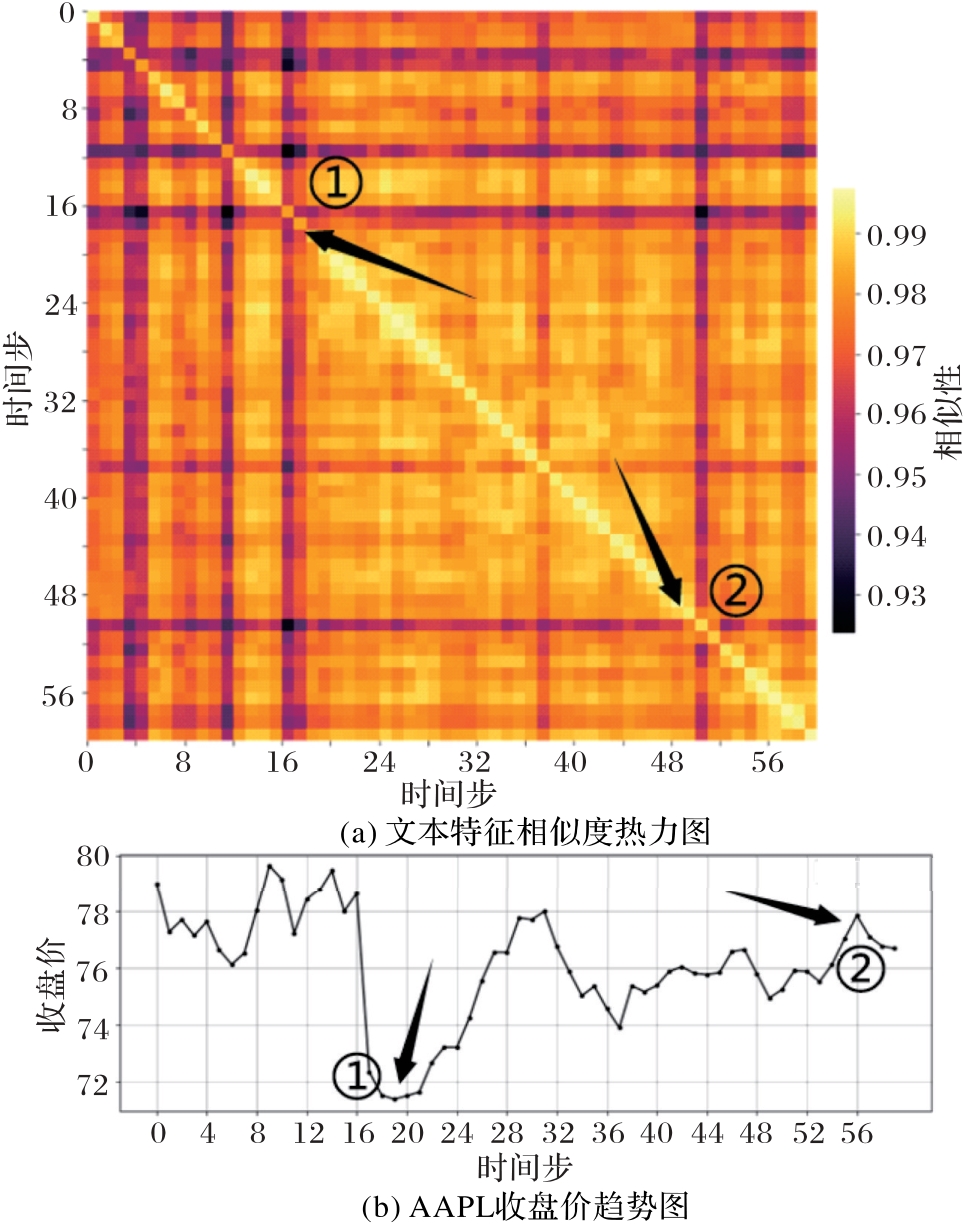

Fig. 1 Visual representation of inter-modal lag

Fig. 2 Architecture of MATCH

| 数据集 | 股票数 | 数据源 | 数据时间区间 | |||

|---|---|---|---|---|---|---|

| 时序 | 文本 | 训练 | 推理 | 测试 | ||

| S&P 500 | 87 | Yahoo Finance | 2014-01-01 to 2014-12-31 | 2015-01-01 to 2015-10-01 | 2015-10-01 to 2015-12-31 | |

| CMIN-US | 110 | Google Finance | Yahoo | 2018-01-02 to 2020-10-15 | 2020-10-16 to 2021-03-11 | 2021-03-12 to 2021-12-31 |

Tab. 1 Statistical information of experimental datasets

| 数据集 | 股票数 | 数据源 | 数据时间区间 | |||

|---|---|---|---|---|---|---|

| 时序 | 文本 | 训练 | 推理 | 测试 | ||

| S&P 500 | 87 | Yahoo Finance | 2014-01-01 to 2014-12-31 | 2015-01-01 to 2015-10-01 | 2015-10-01 to 2015-12-31 | |

| CMIN-US | 110 | Google Finance | Yahoo | 2018-01-02 to 2020-10-15 | 2020-10-16 to 2021-03-11 | 2021-03-12 to 2021-12-31 |

| 模型 | S&P 500 | CMIN⁃US | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | |

| Autoformer | 0.072 2 | 0.059 7 | 0.788 5 | 0.351 5 | 0.038 7 | 0.717 3 | 0.609 1 | 0.284 3 | ||

| DLinear | 0.059 6 | 0.045 5 | 0.673 0 | 0.537 9 | 0.417 4 | 0.021 5 | 0.039 0 | 0.518 1 | 0.502 8 | 0.344 0 |

| PatchTST | 0.070 7 | 0.054 2 | 0.797 2 | 0.666 8 | 0.745 6 | 0.049 4 | 0.032 9 | 0.608 8 | 0.616 2 | 0.689 1 |

| iTransformer | 0.043 6 | 0.025 7 | 0.545 0 | 0.352 5 | 0.761 9 | 0.035 1 | 0.027 6 | 0.615 5 | 0.505 4 | 0.732 0 |

| Adv-ALSTM | 0.071 4 | 0.036 1 | 0.828 1 | 0.871 8 | 0.066 3 | 0.036 2 | 0.711 6 | |||

| ESTIMATE | 0.115 3 | 0.901 7 | 0.894 3 | 0.036 1 | 0.735 4 | 0.763 3 | ||||

| MATCH | 0.090 1 | 1.151 9 | 1.102 3 | 1.356 0 | 0.081 9 | 0.049 3 | 0.857 7 | 0.831 1 | 0.906 2 | |

Tab. 2 Comparison of experimental results on CMIN-US and S&P 500 datasets

| 模型 | S&P 500 | CMIN⁃US | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | |

| Autoformer | 0.072 2 | 0.059 7 | 0.788 5 | 0.351 5 | 0.038 7 | 0.717 3 | 0.609 1 | 0.284 3 | ||

| DLinear | 0.059 6 | 0.045 5 | 0.673 0 | 0.537 9 | 0.417 4 | 0.021 5 | 0.039 0 | 0.518 1 | 0.502 8 | 0.344 0 |

| PatchTST | 0.070 7 | 0.054 2 | 0.797 2 | 0.666 8 | 0.745 6 | 0.049 4 | 0.032 9 | 0.608 8 | 0.616 2 | 0.689 1 |

| iTransformer | 0.043 6 | 0.025 7 | 0.545 0 | 0.352 5 | 0.761 9 | 0.035 1 | 0.027 6 | 0.615 5 | 0.505 4 | 0.732 0 |

| Adv-ALSTM | 0.071 4 | 0.036 1 | 0.828 1 | 0.871 8 | 0.066 3 | 0.036 2 | 0.711 6 | |||

| ESTIMATE | 0.115 3 | 0.901 7 | 0.894 3 | 0.036 1 | 0.735 4 | 0.763 3 | ||||

| MATCH | 0.090 1 | 1.151 9 | 1.102 3 | 1.356 0 | 0.081 9 | 0.049 3 | 0.857 7 | 0.831 1 | 0.906 2 | |

| 模型 | S&P 500 | CMIN⁃US | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | |

| MATCH-v0 | 0.045 4 | 0.026 4 | 0.582 4 | 0.307 7 | 0.908 3 | 0.051 7 | 0.025 8 | 0.601 9 | 0.698 4 | 0.745 7 |

| MATCH-v1 | 0.082 9 | 1.012 5 | 1.003 1 | 0.067 9 | 0.842 2 | 0.758 9 | 0.739 5 | |||

| MATCH-v2 | 0.080 1 | 1.442 2 | 1.247 1 | 0.928 3 | 0.046 7 | 0.862 1 | ||||

| MATCH | 0.090 1 | 0.086 9 | 1.356 0 | 0.081 9 | 0.049 3 | 0.831 1 | 0.906 2 | |||

Tab. 3 Comparison of ablation experimental results

| 模型 | S&P 500 | CMIN⁃US | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | IC(↑) | RIC(↑) | ICIR(↑) | RICIR(↑) | SR(↑) | |

| MATCH-v0 | 0.045 4 | 0.026 4 | 0.582 4 | 0.307 7 | 0.908 3 | 0.051 7 | 0.025 8 | 0.601 9 | 0.698 4 | 0.745 7 |

| MATCH-v1 | 0.082 9 | 1.012 5 | 1.003 1 | 0.067 9 | 0.842 2 | 0.758 9 | 0.739 5 | |||

| MATCH-v2 | 0.080 1 | 1.442 2 | 1.247 1 | 0.928 3 | 0.046 7 | 0.862 1 | ||||

| MATCH | 0.090 1 | 0.086 9 | 1.356 0 | 0.081 9 | 0.049 3 | 0.831 1 | 0.906 2 | |||

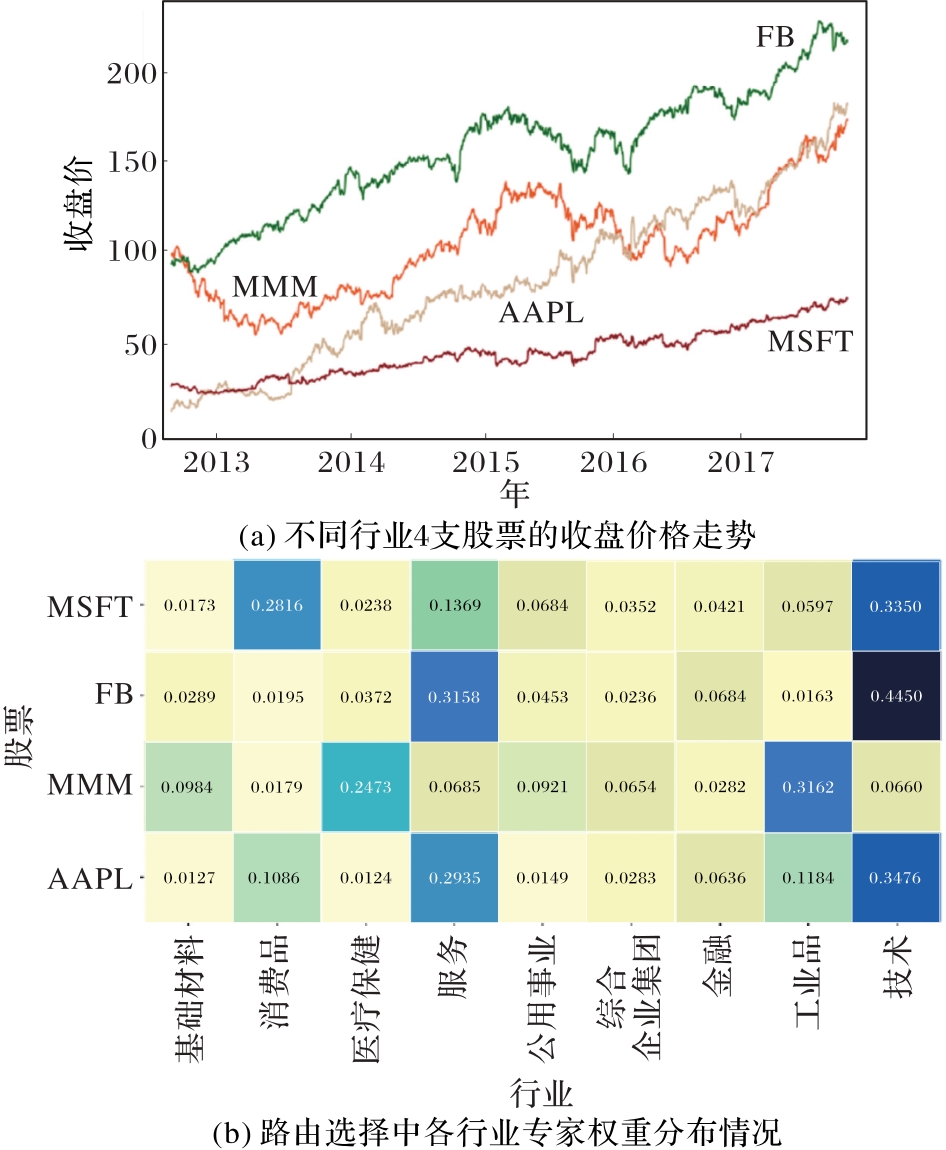

Fig. 3 Visualization of dynamic expert routing weights

Fig. 4 Impact of key components on performance of different stocks

| [1] | 陈榕,任崇广,王智远,等. 基于注意力机制的CRNN文本分类算法[J]. 计算机工程与设计, 2019, 40(11): 3151-3157. |

| CHEN R, REN C G, WANG Z Y, et al. Attention based CRNN for text classification[J]. Computer Engineering and Design, 2019, 40(11): 3151-3157. | |

| [2] | 王慧斌,胡展傲,胡节,等. 基于分段注意力机制的时间序列预测模型[J]. 计算机应用, 2025, 45(7): 2262-2268. |

| WANG H B, HU Z A, HU J, et al. Time series forecasting model based on segmented attention mechanism[J]. Journal of Computer Applications, 2025, 45(7): 2262-2268. | |

| [3] | 李岚皓,严皓钧,周号益,等. 基于神经网络的多尺度信息融合时间序列长期预测模型[J]. 计算机应用, 2025, 45(6): 1776-1783. |

| LI L H, YAN H J, ZHOU H Y, et al. Multi-scale information fusion time series long-term forecasting model based on neural network[J]. Journal of Computer Applications, 2025, 45(6): 1776-1783. | |

| [4] | 王泉,陆啟想,施珮. 用于交通流量预测的多图扩散注意力网络[J]. 计算机应用, 2025, 45(5): 1472-1479. |

| WANG Q, LU Q X, SHI P. Multi-graph diffusion attention networks for traffic flow prediction[J]. Journal of Computer Applications, 2025, 45(5): 1472-1479. | |

| [5] | BALL R, BROWN P. An empirical evaluation of accounting[J]. Journal of Accounting Research, 1968, 6(2): 159-178. |

| [6] | BAKER S R, BLOOM N, DAVIS S J. Measuring economic policy uncertainty[J]. The Quarterly Journal of Economics, 2016, 131(4): 1593-1636. |

| [7] | PÁSTOR Ľ, VERONESI P. Political uncertainty and risk premia[J]. Journal of Financial Economics, 2013, 110(3): 520-545. |

| [8] | GROSSMAN S J, STIGLITZ J E. On the impossibility of informationally efficient markets[J]. The American Economic Review, 1980, 70(3): 393-408. |

| [9] | SHI B, HSU W N, LAKHOTIA K, et al. Learning audio-visual speech representation by masked multimodal cluster prediction[EB/OL]. [2025-06-10].. |

| [10] | GAVRILYUK K, SANFORD R, JAVAN M, et al. Actor-Transformers for group activity recognition[C]// Proceedings of the 2020 IEEE/CVF Conference on Computer Vision and Pattern Recognition. Piscataway: IEEE, 2020: 836-845. |

| [11] | HOCHREITER S, SCHMIDHUBER J. Long short-term memory[J]. Neural Computation, 1997, 9(8): 1735-1780. |

| [12] | SALINAS D, FLUNKERT V, GASTHAUS J, et al. DeepAR: probabilistic forecasting with autoregressive recurrent networks[J]. International Journal of Forecasting, 2020, 36(3): 1181-1191. |

| [13] | BAI S, KOLTER J Z, KOLTUN V. An empirical evaluation of generic convolutional and recurrent networks for sequence modeling[EB/OL]. [2025-06-10].. |

| [14] | SCARSELLI F, GORI M, TSOI A C, et al. The graph neural network model[J]. IEEE Transactions on Neural Networks, 2009, 20(1): 61-80. |

| [15] | ZHOU H, ZHANG S, PENG J, et al. Informer: beyond efficient Transformer for long sequence time-series forecasting[C]// Proceedings of the 35th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2021: 11106-11115. |

| [16] | WU H, XU J, WANG J, et al. Autoformer: decomposition transformers with auto-correlation for long-term series forecasting[C]// Advances in Neural Information Processing Systems 34. Red Hook: Curran Associates Inc.. 2021: 22419-22430. |

| [17] | ZHOU T, MA Z, WEN Q, et al. FEDformer: frequency enhanced decomposed Transformer for long-term series forecasting[C]// Proceedings of the 39th International Conference on Machine Learning. New York: JMLR.org, 2022: 27268-27286. |

| [18] | CIRSTEA R G, GUO C, YANG B, et al. Triformer: triangular, variable-specific attentions for long sequence multivariate time series forecasting-full version[C]// Proceedings of the 31st International Joint Conference on Artificial Intelligence. California: ijcai.org, 2022: 1994-2001. |

| [19] | ZHANG Y, YAN J. Crossformer: Transformer utilizing cross-dimension dependency for multivariate time series forecasting[EB/OL]. [2025-06-10].. |

| [20] | NIE Y, NGUYEN N H, SINTHONG P, et al. A time series is worth 64 words: long-term forecasting with Transformers[EB/OL]. [2025-06-10].. |

| [21] | ZENG A, CHEN M, ZHANG L, et al. Are Transformers effective for time series forecasting?[C]// Proceedings of the 37th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2023: 11121-11128. |

| [22] | HU Z, LIU W, BIAN J, et al. Listening to chaotic whispers: a deep learning framework for news-oriented stock trend prediction[C]// Proceedings of the 11th ACM International Conference on Web Search and Data Mining. New York: ACM, 2018: 261-269. |

| [23] | XU Y, COHEN S B. Stock movement prediction from tweets and historical prices[C]// Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). Stroudsburg: ACL, 2018: 1970-1979. |

| [24] | LI S, LIAO W, CHEN Y, et al. PEN: prediction-explanation network to forecast stock price movement with better explainability[C]// Proceedings of the 37th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2023: 5187-5194. |

| [25] | LUO D, LIAO W, LI S, et al. Causality-guided multi- memory interaction network for multivariate stock price movement prediction[C]// Proceedings of the 61st Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). Stroudsburg: ACL, 2023: 12164-12176. |

| [26] | KOA K J L, MA Y, NG R, et al. Diffusion variational autoencoder for tackling stochasticity in multi-step regression stock price prediction[C]// Proceedings of the 32nd ACM International Conference on Information and Knowledge Management. New York: ACM, 2023: 1087-1096. |

| [27] | WANG H, WANG T, LI S, et al. Heterogeneous interactive snapshot network for review-enhanced stock profiling and recommendation[C]// Proceedings of the 31st International Joint Conference on Artificial Intelligence. California: ijcai.org, 2022: 3962-3969. |

| [28] | XIA H, AO H, LI L, et al. CI-STHPAN: pre-trained attention network for stock selection with channel- independent spatio-temporal hypergraph[C]// Proceedings of the 38th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2024: 9187-9195. |

| [29] | ZHAO L, KONG S, SHEN Y. DoubleAdapt: a meta- learning approach to incremental learning for stock trend forecasting[C]// Proceedings of the 29th ACM SIGKDD Conference on Knowledge Discovery and Data Mining. New York: ACM, 2023: 3492-3503. |

| [30] | YOO J, SOUN Y, PARK Y C, et al. Accurate multivariate stock movement prediction via data-axis Transformer with multi-level contexts[C]// Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery and Data Mining. New York: ACM, 2021: 2037-2045. |

| [31] | LI S, SUN Y, LIN Y, et al. CausalStock: deep end- to-end causal discovery for news-driven stock movement prediction[C]// Proceedings of the 38th International Conference on Neural Information Processing Systems. Red Hook: Curran Associates Inc., 2024: 47432-47454. |

| [32] | WU S, İRSOY O, LU S, et al. BloombergGPT: a large language model for finance[EB/OL]. [2025-06-10].. |

| [33] | WANG N, YANG H, WANG C D. FinGPT: instruction tuning benchmark for open-source large language models in financial datasets[EB/OL]. [2025-06-10].. |

| [34] | ZHANG B, YANG H, ZHOU T, et al. Enhancing financial sentiment analysis via retrieval augmented large language models[C]// Proceedings of the 4th ACM International Conference on AI in Finance. New York: ACM, 2023: 349-356. |

| [35] | DONG Z, FAN X, PENG Z. FNSPID: a comprehensive financial news dataset in time series[C]// Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining. New York: ACM, 2024: 4918-4927. |

| [36] | YU X, CHEN Z, LU Y. Harnessing LLMs for temporal data: a study on explainable financial time series forecasting[C]// Proceedings of the 2023 Conference on Empirical Methods in Natural Language Processing: Industry Track. Stroudsburg: ACL, 2023: 739-753. |

| [37] | KOA K J L, MA Y, NG R, et al. Learning to generate explainable stock predictions using self-reflective large language models[C]// Proceedings of the ACM Web Conference 2024. New York: ACM, 2024: 4304-4315. |

| [38] | LI X, SHEN X, ZENG Y, et al. FinReport: explainable stock earnings forecasting via news factor analyzing model[C]// Companion Proceedings of the ACM Web Conference 2024. New York: ACM, 2024: 319-327. |

| [39] | CHEN P, ZHANG Y, CHENG Y, et al. Pathformer: multi- scale transformers with adaptive pathways for time series forecasting[EB/OL]. [2025-06-10].. |

| [40] | HUANG Q, AN Z, ZHUANG N, et al. Harder tasks need more experts: dynamic routing in MoE models[C]// Proceedings of the 62nd Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers). Stroudsburg: ACL, 2024: 12883-12895. |

| [41] | RADFORD A, WU J, CHILD R, et al. Language models are unsupervised multitask learners[EB/OL]. [2025-06-10].. |

| [42] | MIKOLOV T, SUTSKEVER I, CHEN K, et al. Distributed representations of words and phrases and their compositionality[C]// Proceedings of the 27th International Conference on Neural Information Processing Systems. Red Hook: Curran Associates Inc., 2013: 3111-3119. |

| [43] | PENNINGTON J, SOCHER R, MANNING C D. GloVe: global vectors for word representation[C]// Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing. Stroudsburg: ACL, 2014: 1532-1543. |

| [44] | LIU Y, HU T, ZHANG H, et al. iTransformer: inverted Transformers are effective for time series forecasting[EB/OL]. [2025-06-10].. |

| [45] | FENG F, CHEN H, HE X, et al. Enhancing stock movement prediction with adversarial training[C]// Proceedings of the 28th International Joint Conference on Artificial Intelligence. California: ijcai.org, 2019: 5843-5849. |

| [46] | HUYNH T T, NGUYEN M H, NGUYEN T T, et al. Efficient integration of multi-order dynamics and internal dynamics in stock movement prediction[C]// Proceedings of the 16th ACM International Conference on Web Search and Data Mining. New York: ACM, 2023: 850-858. |

| [1] | Junheng WU, Xiaodong WANG, Qixue HE. Time series prediction model based on statistical distribution sensing and frequency domain dual-channel fusion [J]. Journal of Computer Applications, 2026, 46(1): 113-123. |

| [2] | Jinyang HUANG, Fengqi CUI, Changxiu MA, Wendong FAN, Meng LI, Jingyu LI, Xiao SUN, Linsheng HUANG, Zhi LIU. Sleep apnea detection based on universal wristband [J]. Journal of Computer Applications, 2025, 45(9): 3045-3056. |

| [3] | Yihan WANG, Chong LU, Zhongyuan CHEN. Multimodal sentiment analysis model with cross-modal text information enhancement [J]. Journal of Computer Applications, 2025, 45(7): 2237-2244. |

| [4] | Jiaqi CHEN, Yulin HE, Yingchao CHENG, Zhexue HUANG. Semi-EM algorithm for solving Gamma mixture model of multimodal probability distribution [J]. Journal of Computer Applications, 2025, 45(7): 2153-2161. |

| [5] | Zonghang WU, Dong ZHANG, Guanyu LI. Multimodal fusion recommendation algorithm based on joint self-supervised learning [J]. Journal of Computer Applications, 2025, 45(6): 1858-1868. |

| [6] | Qing ZHANG, Fan YANG, Yuhan FANG. Chinese spelling correction algorithm based on multi-modal information fusion [J]. Journal of Computer Applications, 2025, 45(5): 1528-1534. |

| [7] | Haiyan TIAN, Saihao HUANG, Dong ZHANG, Shoushan LI. Visually guided word segmentation and part of speech tagging [J]. Journal of Computer Applications, 2025, 45(5): 1488-1495. |

| [8] | Jiana MENG, Chenhao BAI, Di ZHAO, Bolin WANG, Linlin GAO. Multimodal named entity recognition under causal intervention [J]. Journal of Computer Applications, 2025, 45(12): 3796-3803. |

| [9] | Huilin GUI, Kun YUE, Liang DUAN. Multimodal knowledge graph link prediction method based on fusing image and textual information [J]. Journal of Computer Applications, 2025, 45(11): 3540-3546. |

| [10] | Jinwen LIU, Lei WANG, Bo MA, Rui DONG, Yating YANG, Ahtamjan Ahmat, Xinyue WANG. Multimodal harmful content detection method based on weakly supervised modality semantic enhancement [J]. Journal of Computer Applications, 2025, 45(10): 3146-3153. |

| [11] | Yongping WANG, Yao LIU, Xiaolin ZHANG, Jingyu WANG, Lixin LIU. Multimodal adversarial example generation method for Chinese text classification [J]. Journal of Computer Applications, 2025, 45(10): 3074-3082. |

| [12] | Kaipeng XUE, Tao XU, Chunjie LIAO. Multimodal sentiment analysis network with self-supervision and multi-layer cross attention [J]. Journal of Computer Applications, 2024, 44(8): 2387-2392. |

| [13] | Tian CHEN, Conghu CAI, Xiaohui YUAN, Beibei LUO. Multimodal emotion recognition method based on multiscale convolution and self-attention feature fusion [J]. Journal of Computer Applications, 2024, 44(2): 369-376. |

| [14] | Hua LAI, Tong SUN, Wenjun WANG, Zhengtao YU, Shengxiang GAO, Ling DONG. Text punctuation restoration for Vietnamese speech recognition with multimodal features [J]. Journal of Computer Applications, 2024, 44(2): 418-423. |

| [15] | Shengyou ZHENG, Yanxiang CHEN, Zuxing ZHAO, Haiyang LIU. Construction and benchmark detection of multimodal partial forgery dataset [J]. Journal of Computer Applications, 2024, 44(10): 3134-3140. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||