《计算机应用》唯一官方网站 ›› 2022, Vol. 42 ›› Issue (3): 797-803.DOI: 10.11772/j.issn.1001-9081.2021050748

所属专题: 人工智能; 2021年中国计算机学会人工智能会议(CCFAI 2021)

• 2021年中国计算机学会人工智能会议(CCFAI 2021) • 上一篇 下一篇

李晓杰1, 崔超然1( ), 宋广乐2, 苏雅茜1, 吴天泽3, 张春云1

), 宋广乐2, 苏雅茜1, 吴天泽3, 张春云1

Xiaojie LI1, Chaoran CUI1(), Guangle SONG2, Yaxi SU1, Tianze WU3, Chunyun ZHANG1

摘要:

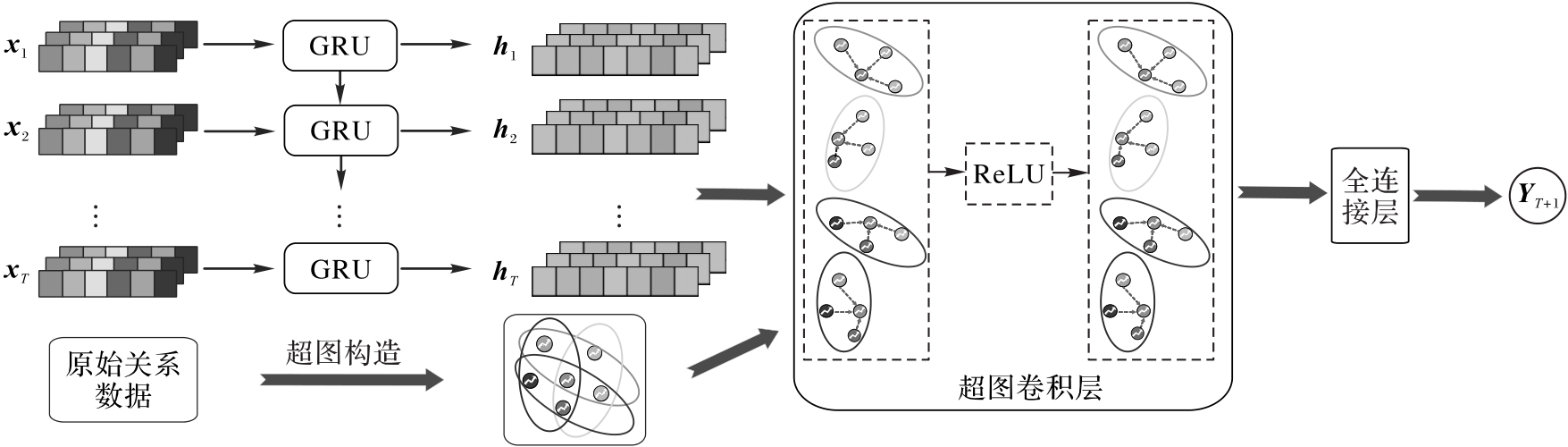

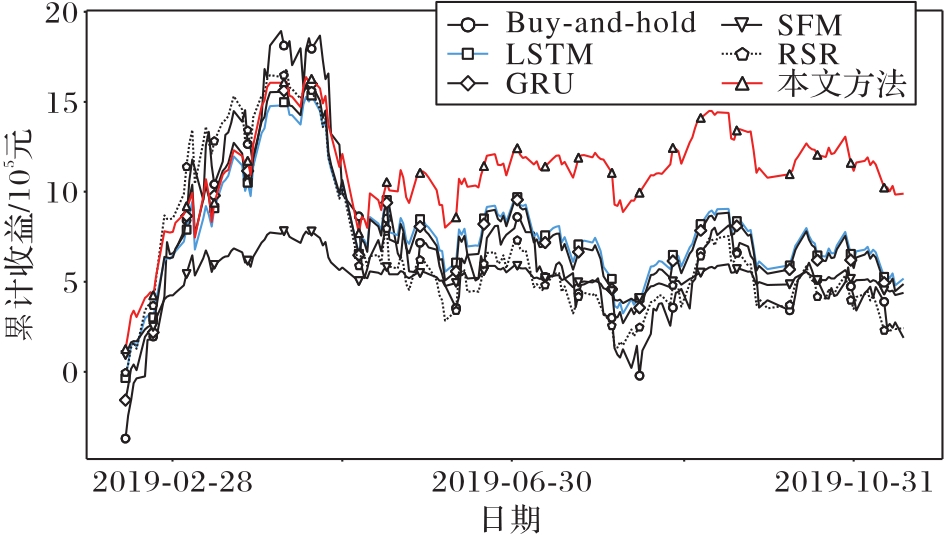

传统的股票预测方法大多基于时间序列模型,忽视了股票之间复杂的关系,并且该关系往往超出成对连接,例如同行业板块内股票或者基金持仓多支股票。针对该问题,提出一种基于时序超图卷积神经网络(HGCN)的股价走势预测方法,根据金融投资事实构造超图模型以拟合股票之间的多元关系,该模型包括两大组件:门控循环单元(GRU)网络和超图卷积神经网络。GRU网络对历史数据进行时间序列建模,捕捉长期依赖关系;HGCN建模股票间的高阶关系以学习内在关系属性,从而将股票间多元关系信息引入到传统的时序建模中,进行端到端的趋势预测。在中国A股市场真实数据集上的实验结果表明,相较于已有的股票预测方法,所提模型预测性能有所提升;如与GRU网络相比,所提模型在ACC和F1_score上的相对增幅分别为9.74%和8.13%,且更具有稳定性。此外,模拟回测结果显示,基于该模型的交易策略更具获利能力,年回报率达到11.30%,与长短期记忆(LSTM)网络相比提高了5个百分点。

中图分类号: