Journal of Computer Applications ›› 2026, Vol. 46 ›› Issue (6): 1863-1871.DOI: 10.11772/j.issn.1001-9081.2025060707

• Data science and technology • Previous Articles Next Articles

Xinru LIU1, Songhua LIU2( ), Lusha QI2, Yaofei MENG2

), Lusha QI2, Yaofei MENG2

Received:2025-06-24

Revised:2025-10-05

Accepted:2025-10-16

Online:2025-10-23

Published:2026-06-10

Contact:

Songhua LIU

About author:LIU Xinru, born in 2000, M. S. candidate. Her research interests include time series forecasting, ensemble learning.Supported by:

刘新如1, 刘松华2(), 祁露莎2, 孟耀飞2

通讯作者:

刘松华

作者简介:刘新如(2000—),女,河南开封人,硕士研究生,CCF会员,主要研究方向:时序预测、集成学习基金资助:CLC Number:

Xinru LIU, Songhua LIU, Lusha QI, Yaofei MENG. Time series forecasting model based on dynamic weighted ensemble[J]. Journal of Computer Applications, 2026, 46(6): 1863-1871.

刘新如, 刘松华, 祁露莎, 孟耀飞. 基于动态加权集成的时序预测模型[J]. 《计算机应用》唯一官方网站, 2026, 46(6): 1863-1871.

Add to citation manager EndNote|Ris|BibTeX

URL: https://www.joca.cn/EN/10.11772/j.issn.1001-9081.2025060707

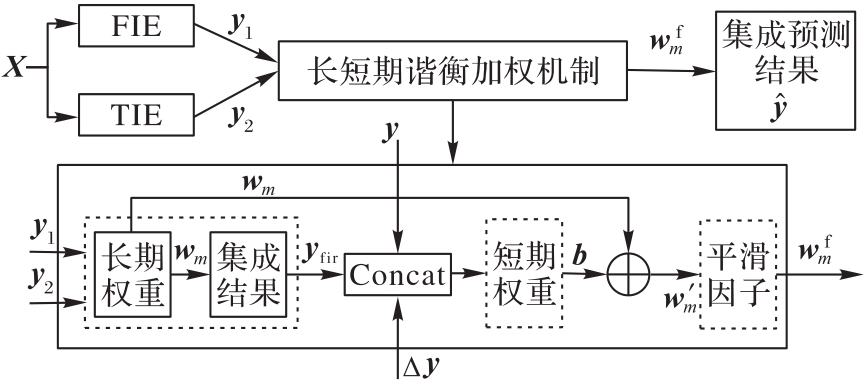

Fig. 1 Architecture of TFEM model

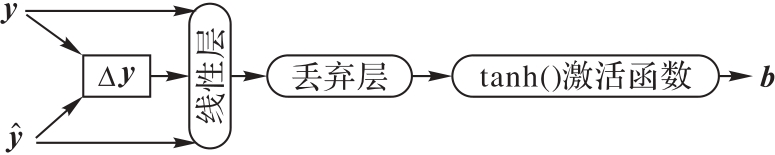

Fig. 2 Structure of short-term weighting mechanism

| 数据集 | 属性数 | 时间步 | 粒度/min |

|---|---|---|---|

| ETTh1,ETTh2 | 7 | 17 420 | 60 |

| ETTm1,ETTm1 | 7 | 69 680 | 15 |

| Weather | 21 | 52 696 | 10 |

| Exchange_Rate | 8 | 7 588 | 1 440 |

| ILI | 7 | 966 | 10 080 |

Tab. 1 Basic information of datasets

| 数据集 | 属性数 | 时间步 | 粒度/min |

|---|---|---|---|

| ETTh1,ETTh2 | 7 | 17 420 | 60 |

| ETTm1,ETTm1 | 7 | 69 680 | 15 |

| Weather | 21 | 52 696 | 10 |

| Exchange_Rate | 8 | 7 588 | 1 440 |

| ILI | 7 | 966 | 10 080 |

| 数据集 | 预测 长度 | TFEM | DLinear | PatchTST | iTransformer | TimesNet | ATFNet | OneNet | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | ||

| ETTh1 | 96 | 0.268 | 0.345 | 0.375 | 0.399 | 0.370 | 0.400 | 0.386 | 0.405 | 0.384 | 0.402 | 0.405 | 0.442 | ||

| 192 | 0.284 | 0.355 | 0.405 | 0.416 | 0.413 | 0.429 | 0.441 | 0.436 | 0.436 | 0.429 | 0.467 | 0.482 | |||

| 336 | 0.284 | 0.358 | 0.439 | 0.443 | 0.422 | 0.440 | 0.487 | 0.458 | 0.491 | 0.469 | 0.514 | 0.521 | |||

| 720 | 0.280 | 0.356 | 0.472 | 0.490 | 0.447 | 0.468 | 0.503 | 0.491 | 0.521 | 0.500 | 0.614 | 0.589 | |||

| ETTh2 | 96 | 0.289 | 0.353 | 0.274 | 0.337 | 0.297 | 0.349 | 0.340 | 0.374 | 0.171 | 0.282 | 0.096 | 0.218 | ||

| 192 | 0.128 | 0.244 | 0.383 | 0.418 | 0.341 | 0.382 | 0.380 | 0.400 | 0.402 | 0.414 | 0.211 | 0.315 | |||

| 336 | 0.136 | 0.253 | 0.448 | 0.465 | 0.329 | 0.384 | 0.428 | 0.432 | 0.452 | 0.452 | 0.236 | 0.344 | |||

| 720 | 0.138 | 0.255 | 0.605 | 0.551 | 0.379 | 0.422 | 0.427 | 0.445 | 0.462 | 0.468 | 0.297 | 0.399 | |||

| ETTm1 | 96 | 0.105 | 0.224 | 0.299 | 0.343 | 0.293 | 0.346 | 0.334 | 0.368 | 0.338 | 0.375 | 0.327 | 0.375 | ||

| 192 | 0.112 | 0.232 | 0.335 | 0.365 | 0.333 | 0.370 | 0.377 | 0.391 | 0.374 | 0.487 | 0.370 | 0.412 | |||

| 336 | 0.117 | 0.238 | 0.369 | 0.386 | 0.369 | 0.392 | 0.426 | 0.420 | 0.410 | 0.411 | 0.402 | 0.438 | |||

| 720 | 0.131 | 0.251 | 0.425 | 0.421 | 0.416 | 0.420 | 0.491 | 0.459 | 0.478 | 0.450 | 0.453 | 0.476 | |||

| ETTm2 | 96 | 0.057 | 0.157 | 0.167 | 0.260 | 0.166 | 0.256 | 0.180 | 0.264 | 0.187 | 0.267 | 0.114 | 0.227 | ||

| 192 | 0.059 | 0.160 | 0.224 | 0.303 | 0.223 | 0.296 | 0.250 | 0.309 | 0.249 | 0.309 | 0.141 | 0.254 | |||

| 336 | 0.062 | 0.163 | 0.280 | 0.334 | 0.274 | 0.329 | 0.311 | 0.348 | 0.321 | 0.351 | 0.172 | 0.281 | |||

| 720 | 0.068 | 0.172 | 0.364 | 0.385 | 0.362 | 0.385 | 0.412 | 0.407 | 0.408 | 0.403 | 0.219 | 0.317 | |||

| Weather | 96 | 0.064 | 0.098 | 0.176 | 0.237 | 0.149 | 0.198 | 0.174 | 0.214 | 0.172 | 0.220 | 0.156 | 0.206 | ||

| 192 | 0.064 | 0.100 | 0.220 | 0.282 | 0.194 | 0.241 | 0.221 | 0.254 | 0.219 | 0.261 | 0.199 | 0.246 | |||

| 336 | 0.066 | 0.101 | 0.265 | 0.319 | 0.245 | 0.282 | 0.278 | 0.296 | 0.280 | 0.306 | 0.249 | 0.286 | |||

| 720 | 0.070 | 0.104 | 0.323 | 0.362 | 0.314 | 0.334 | 0.358 | 0.347 | 0.365 | 0.359 | 0.311 | 0.335 | |||

| Exchange_Rate | 96 | 0.016 | 0.083 | 0.084 | 0.216 | 0.091 | 0.208 | 0.086 | 0.206 | 0.107 | 0.234 | 0.097 | 0.219 | ||

| 192 | 0.019 | 0.090 | 0.157 | 0.298 | 0.175 | 0.298 | 0.177 | 0.299 | 0.226 | 0.344 | 0.239 | 0.342 | |||

| 336 | 0.018 | 0.087 | 0.236 | 0.379 | 0.355 | 0.425 | 0.331 | 0.417 | 0.367 | 0.448 | 0.367 | 0.445 | |||

| 720 | 0.042 | 0.105 | 0.626 | 0.634 | 0.974 | 0.733 | 0.847 | 0.691 | 0.964 | 0.746 | 0.645 | 0.611 | |||

| ILI | 24 | 0.928 | 0.666 | 3.015 | 1.192 | 1.500 | 0.823 | 2.317 | 0.934 | 1.543 | 0.798 | 1.481 | 0.783 | ||

| 36 | 0.934 | 0.657 | 2.737 | 1.036 | 1.579 | 0.870 | 1.482 | 0.812 | 1.972 | 0.920 | 1.607 | 0.825 | |||

| 48 | 0.967 | 0.672 | 2.577 | 1.043 | 1.553 | 0.815 | 1.607 | 0.862 | 2.238 | 0.940 | 1.650 | 0.844 | |||

| 60 | 0.944 | 0.660 | 2.821 | 1.091 | 1.470 | 1.882 | 0.969 | 2.027 | 0.928 | 2.156 | 1.014 | 0.836 | |||

Tab. 2 Prediction errors of various models on benchmark datasets

| 数据集 | 预测 长度 | TFEM | DLinear | PatchTST | iTransformer | TimesNet | ATFNet | OneNet | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | ||

| ETTh1 | 96 | 0.268 | 0.345 | 0.375 | 0.399 | 0.370 | 0.400 | 0.386 | 0.405 | 0.384 | 0.402 | 0.405 | 0.442 | ||

| 192 | 0.284 | 0.355 | 0.405 | 0.416 | 0.413 | 0.429 | 0.441 | 0.436 | 0.436 | 0.429 | 0.467 | 0.482 | |||

| 336 | 0.284 | 0.358 | 0.439 | 0.443 | 0.422 | 0.440 | 0.487 | 0.458 | 0.491 | 0.469 | 0.514 | 0.521 | |||

| 720 | 0.280 | 0.356 | 0.472 | 0.490 | 0.447 | 0.468 | 0.503 | 0.491 | 0.521 | 0.500 | 0.614 | 0.589 | |||

| ETTh2 | 96 | 0.289 | 0.353 | 0.274 | 0.337 | 0.297 | 0.349 | 0.340 | 0.374 | 0.171 | 0.282 | 0.096 | 0.218 | ||

| 192 | 0.128 | 0.244 | 0.383 | 0.418 | 0.341 | 0.382 | 0.380 | 0.400 | 0.402 | 0.414 | 0.211 | 0.315 | |||

| 336 | 0.136 | 0.253 | 0.448 | 0.465 | 0.329 | 0.384 | 0.428 | 0.432 | 0.452 | 0.452 | 0.236 | 0.344 | |||

| 720 | 0.138 | 0.255 | 0.605 | 0.551 | 0.379 | 0.422 | 0.427 | 0.445 | 0.462 | 0.468 | 0.297 | 0.399 | |||

| ETTm1 | 96 | 0.105 | 0.224 | 0.299 | 0.343 | 0.293 | 0.346 | 0.334 | 0.368 | 0.338 | 0.375 | 0.327 | 0.375 | ||

| 192 | 0.112 | 0.232 | 0.335 | 0.365 | 0.333 | 0.370 | 0.377 | 0.391 | 0.374 | 0.487 | 0.370 | 0.412 | |||

| 336 | 0.117 | 0.238 | 0.369 | 0.386 | 0.369 | 0.392 | 0.426 | 0.420 | 0.410 | 0.411 | 0.402 | 0.438 | |||

| 720 | 0.131 | 0.251 | 0.425 | 0.421 | 0.416 | 0.420 | 0.491 | 0.459 | 0.478 | 0.450 | 0.453 | 0.476 | |||

| ETTm2 | 96 | 0.057 | 0.157 | 0.167 | 0.260 | 0.166 | 0.256 | 0.180 | 0.264 | 0.187 | 0.267 | 0.114 | 0.227 | ||

| 192 | 0.059 | 0.160 | 0.224 | 0.303 | 0.223 | 0.296 | 0.250 | 0.309 | 0.249 | 0.309 | 0.141 | 0.254 | |||

| 336 | 0.062 | 0.163 | 0.280 | 0.334 | 0.274 | 0.329 | 0.311 | 0.348 | 0.321 | 0.351 | 0.172 | 0.281 | |||

| 720 | 0.068 | 0.172 | 0.364 | 0.385 | 0.362 | 0.385 | 0.412 | 0.407 | 0.408 | 0.403 | 0.219 | 0.317 | |||

| Weather | 96 | 0.064 | 0.098 | 0.176 | 0.237 | 0.149 | 0.198 | 0.174 | 0.214 | 0.172 | 0.220 | 0.156 | 0.206 | ||

| 192 | 0.064 | 0.100 | 0.220 | 0.282 | 0.194 | 0.241 | 0.221 | 0.254 | 0.219 | 0.261 | 0.199 | 0.246 | |||

| 336 | 0.066 | 0.101 | 0.265 | 0.319 | 0.245 | 0.282 | 0.278 | 0.296 | 0.280 | 0.306 | 0.249 | 0.286 | |||

| 720 | 0.070 | 0.104 | 0.323 | 0.362 | 0.314 | 0.334 | 0.358 | 0.347 | 0.365 | 0.359 | 0.311 | 0.335 | |||

| Exchange_Rate | 96 | 0.016 | 0.083 | 0.084 | 0.216 | 0.091 | 0.208 | 0.086 | 0.206 | 0.107 | 0.234 | 0.097 | 0.219 | ||

| 192 | 0.019 | 0.090 | 0.157 | 0.298 | 0.175 | 0.298 | 0.177 | 0.299 | 0.226 | 0.344 | 0.239 | 0.342 | |||

| 336 | 0.018 | 0.087 | 0.236 | 0.379 | 0.355 | 0.425 | 0.331 | 0.417 | 0.367 | 0.448 | 0.367 | 0.445 | |||

| 720 | 0.042 | 0.105 | 0.626 | 0.634 | 0.974 | 0.733 | 0.847 | 0.691 | 0.964 | 0.746 | 0.645 | 0.611 | |||

| ILI | 24 | 0.928 | 0.666 | 3.015 | 1.192 | 1.500 | 0.823 | 2.317 | 0.934 | 1.543 | 0.798 | 1.481 | 0.783 | ||

| 36 | 0.934 | 0.657 | 2.737 | 1.036 | 1.579 | 0.870 | 1.482 | 0.812 | 1.972 | 0.920 | 1.607 | 0.825 | |||

| 48 | 0.967 | 0.672 | 2.577 | 1.043 | 1.553 | 0.815 | 1.607 | 0.862 | 2.238 | 0.940 | 1.650 | 0.844 | |||

| 60 | 0.944 | 0.660 | 2.821 | 1.091 | 1.470 | 1.882 | 0.969 | 2.027 | 0.928 | 2.156 | 1.014 | 0.836 | |||

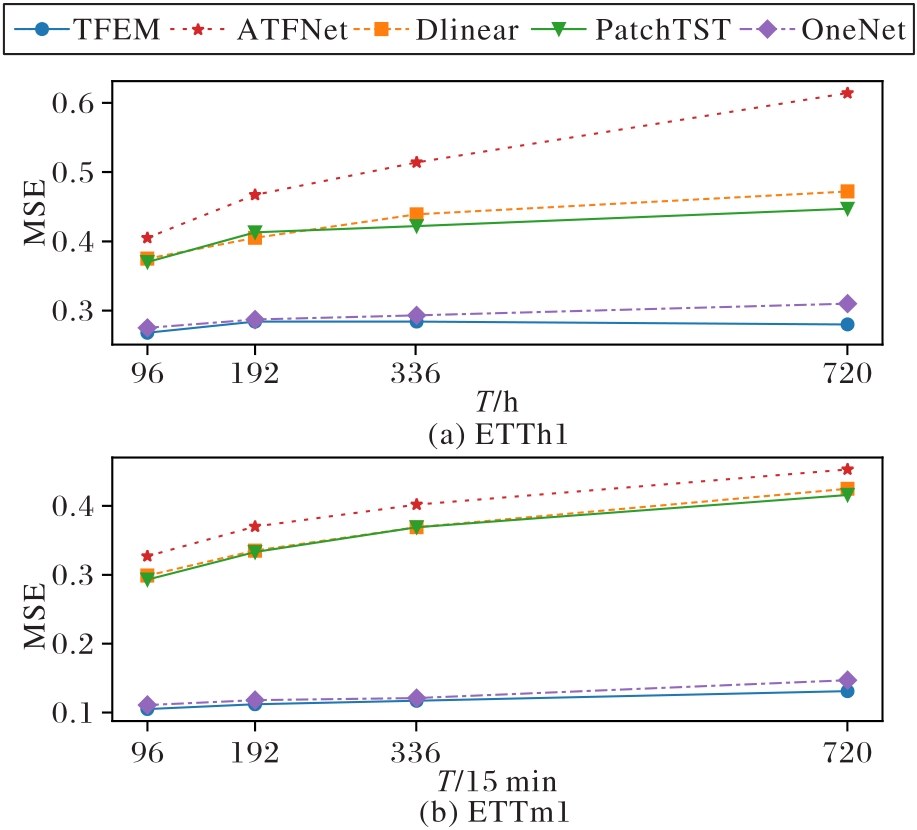

Fig.3 MSEs of TFEM and some representative models under different prediction lengths

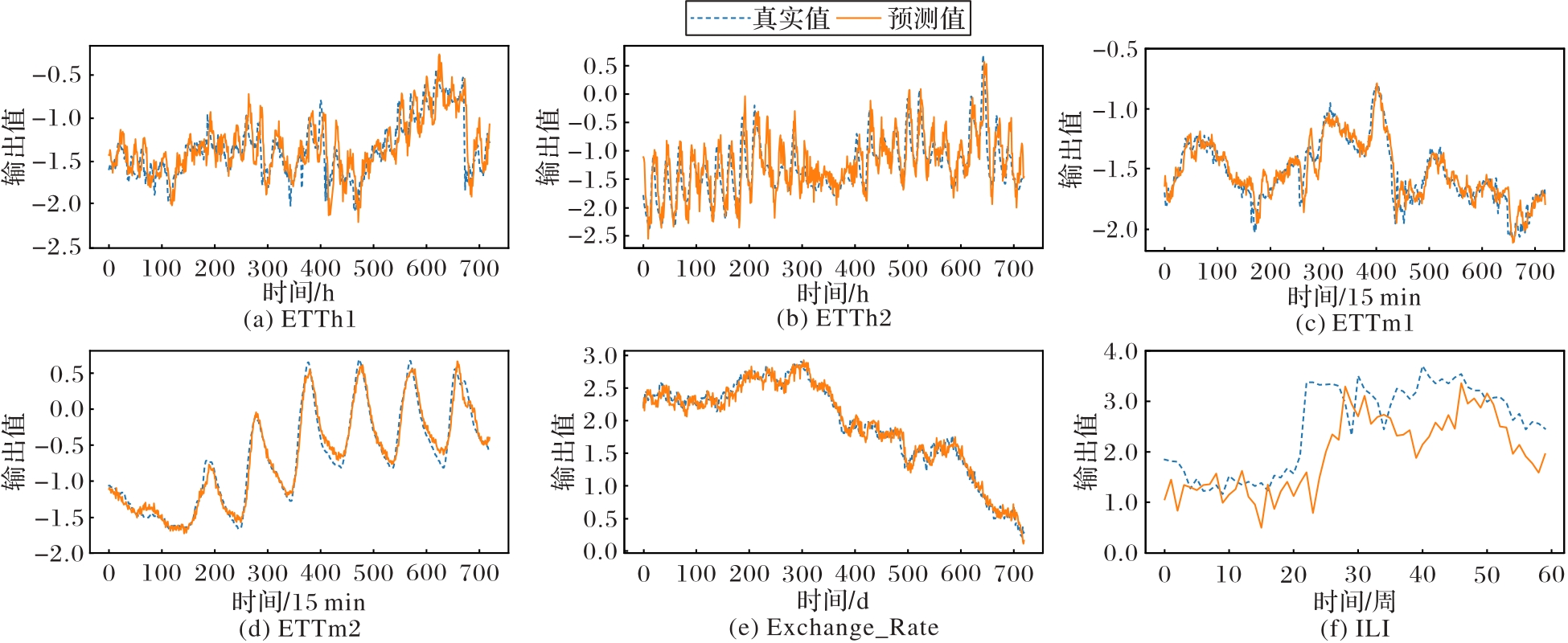

Fig. 4 Prediction performance of TFEM on various datasets

| 数据集 | 概率值 | ADF 统计量 | 临界值 (1%) | 临界值 (5%) | 临界值 (10%) | 结论 |

|---|---|---|---|---|---|---|

| Exchange_Rate | 0.42 | -1.73 | -3.43 | -2.86 | -2.57 | 非平稳 |

| ILI | 0.76 | -0.98 | -3.43 | -2.86 | -2.57 | 非平稳 |

Tab. 3 ADF test results

| 数据集 | 概率值 | ADF 统计量 | 临界值 (1%) | 临界值 (5%) | 临界值 (10%) | 结论 |

|---|---|---|---|---|---|---|

| Exchange_Rate | 0.42 | -1.73 | -3.43 | -2.86 | -2.57 | 非平稳 |

| ILI | 0.76 | -0.98 | -3.43 | -2.86 | -2.57 | 非平稳 |

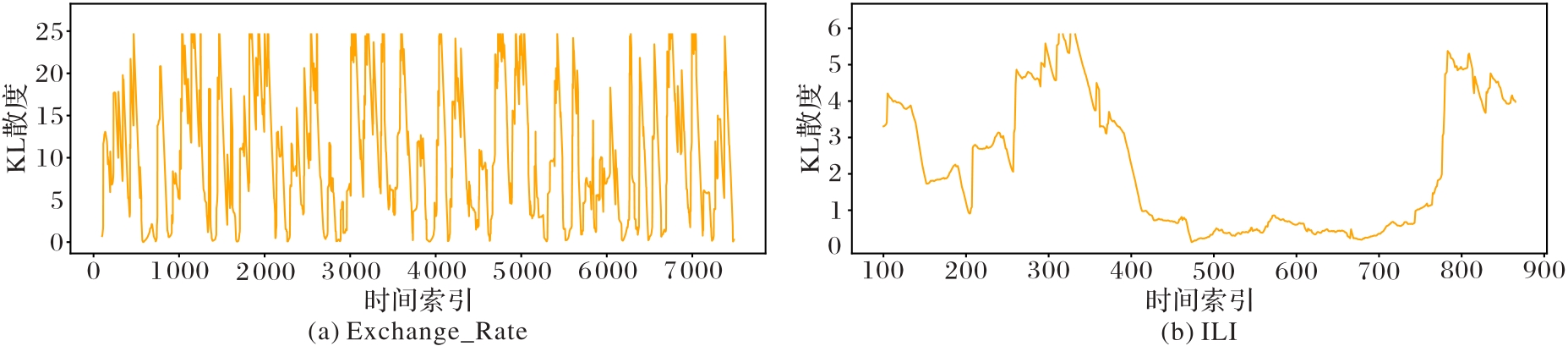

Fig. 5 KL divergence changes on Exchange_Rate and ILI datasets

| 机制 | 计算量/109 | 参数量/103 | 时间/ms | 内存/MB |

|---|---|---|---|---|

| LRSA | 0.40 | 131.8 | 0.81 | 24 |

| MHSA | 3.22 | 1 050.6 | 1.18 | 28 |

Tab. 4 Efficiency comparison between low-rank and standard self-attention mechanisms

| 机制 | 计算量/109 | 参数量/103 | 时间/ms | 内存/MB |

|---|---|---|---|---|

| LRSA | 0.40 | 131.8 | 0.81 | 24 |

| MHSA | 3.22 | 1 050.6 | 1.18 | 28 |

| 模型 | 时间复杂度 | 模型 | 时间复杂度 |

|---|---|---|---|

| TFEM | ATFNet | ||

| PatchTST | OneNet | ||

| DLinear |

Tab. 5 Time complexity of different models

| 模型 | 时间复杂度 | 模型 | 时间复杂度 |

|---|---|---|---|

| TFEM | ATFNet | ||

| PatchTST | OneNet | ||

| DLinear |

| 模型 | 参数量/106 | 时间/s | 内存/GB | MSE |

|---|---|---|---|---|

| TFEM | 28.20 | 3.900 00 | 0.48 | 0.23 |

| PatchTST | 40.99 | 3.060 00 | 0.40 | 0.49 |

| DLinear | 0.53 | 0.000 34 | 0.02 | 0.68 |

| ATFNet | 143.30 | 10.620 00 | 1.20 | 0.51 |

| OneNet | 92.27 | 7.880 00 | 0.93 | 0.31 |

Tab. 6 Spatial-temporal overhead and prediction performance of different models

| 模型 | 参数量/106 | 时间/s | 内存/GB | MSE |

|---|---|---|---|---|

| TFEM | 28.20 | 3.900 00 | 0.48 | 0.23 |

| PatchTST | 40.99 | 3.060 00 | 0.40 | 0.49 |

| DLinear | 0.53 | 0.000 34 | 0.02 | 0.68 |

| ATFNet | 143.30 | 10.620 00 | 1.20 | 0.51 |

| OneNet | 92.27 | 7.880 00 | 0.93 | 0.31 |

| 数据集 | 预测长度 | TFEM | -W | -b | -EMA | ||||

|---|---|---|---|---|---|---|---|---|---|

| MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | ||

| ETTh1 | 96 | 0.268 | 0.345 | 0.285 | 0.352 | 0.336 | 0.377 | ||

| 192 | 0.284 | 0.355 | 0.307 | 0.367 | 0.359 | 0.391 | |||

| 336 | 0.284 | 0.358 | 0.326 | 0.374 | 0.368 | 0.396 | |||

| 720 | 0.280 | 0.356 | 0.310 | 0.372 | 0.382 | 0.412 | |||

| ETTh2 | 96 | 0.122 | 0.238 | 0.141 | 0.251 | 0.186 | 0.286 | ||

| 192 | 0.128 | 0.244 | 0.155 | 0.264 | 0.193 | 0.293 | |||

| 336 | 0.136 | 0.253 | 0.158 | 0.268 | 0.406 | 0.430 | |||

| 720 | 0.138 | 0.255 | 0.280 | 0.362 | 0.356 | 0.399 | |||

| Weather | 96 | 0.064 | 0.098 | 0.079 | 0.161 | 0.225 | 0.203 | ||

| 192 | 0.064 | 0.100 | 0.085 | 0.173 | 0.231 | 0.232 | |||

| 336 | 0.066 | 0.101 | 0.093 | 0.162 | 0.221 | 0.243 | |||

| 720 | 0.070 | 0.104 | 0.102 | 0.151 | 0.211 | 0.263 | |||

Tab. 7 Ablation experiment results on ensemble strategies

| 数据集 | 预测长度 | TFEM | -W | -b | -EMA | ||||

|---|---|---|---|---|---|---|---|---|---|

| MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | ||

| ETTh1 | 96 | 0.268 | 0.345 | 0.285 | 0.352 | 0.336 | 0.377 | ||

| 192 | 0.284 | 0.355 | 0.307 | 0.367 | 0.359 | 0.391 | |||

| 336 | 0.284 | 0.358 | 0.326 | 0.374 | 0.368 | 0.396 | |||

| 720 | 0.280 | 0.356 | 0.310 | 0.372 | 0.382 | 0.412 | |||

| ETTh2 | 96 | 0.122 | 0.238 | 0.141 | 0.251 | 0.186 | 0.286 | ||

| 192 | 0.128 | 0.244 | 0.155 | 0.264 | 0.193 | 0.293 | |||

| 336 | 0.136 | 0.253 | 0.158 | 0.268 | 0.406 | 0.430 | |||

| 720 | 0.138 | 0.255 | 0.280 | 0.362 | 0.356 | 0.399 | |||

| Weather | 96 | 0.064 | 0.098 | 0.079 | 0.161 | 0.225 | 0.203 | ||

| 192 | 0.064 | 0.100 | 0.085 | 0.173 | 0.231 | 0.232 | |||

| 336 | 0.066 | 0.101 | 0.093 | 0.162 | 0.221 | 0.243 | |||

| 720 | 0.070 | 0.104 | 0.102 | 0.151 | 0.211 | 0.263 | |||

| r | 参数量/106 | 推理时间/s | 内存/GB | MSE |

|---|---|---|---|---|

| 8 | 27.12 | 3.65 | 0.463 | 0.253 |

| 16 | 27.93 | 3.79 | 0.476 | 0.236 |

| 32 | 28.20 | 3.90 | 0.480 | 0.230 |

| 64 | 29.47 | 4.17 | 0.494 | 0.227 |

Tab. 8 Spatio-temporal overhead and performance under different r

| r | 参数量/106 | 推理时间/s | 内存/GB | MSE |

|---|---|---|---|---|

| 8 | 27.12 | 3.65 | 0.463 | 0.253 |

| 16 | 27.93 | 3.79 | 0.476 | 0.236 |

| 32 | 28.20 | 3.90 | 0.480 | 0.230 |

| 64 | 29.47 | 4.17 | 0.494 | 0.227 |

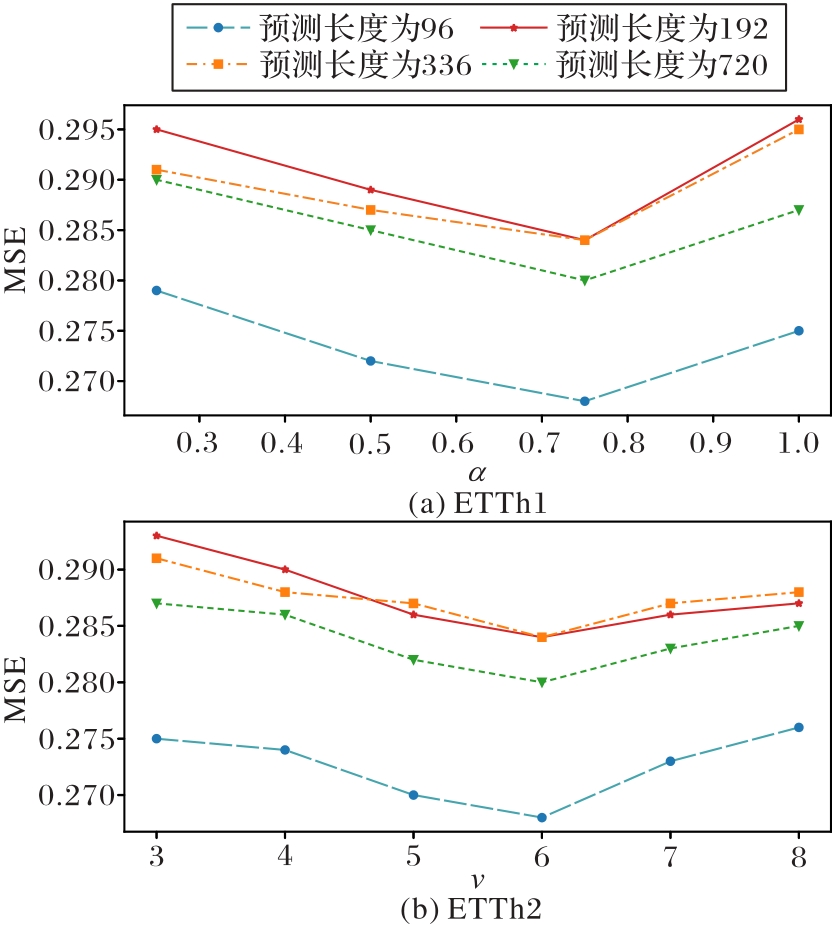

Fig.6 Impact of hyperparameters α and v on model performance

| [1] | 宋凌云,马卓源,李战怀,等. 面向金融风险预测的时序图神经网络综述[J]. 软件学报, 2024, 35(8): 3897-3922. |

| SONG L Y, MA Z Y, LI Z H, et al. Review on temporal graph neural networks for financial risk prediction[J]. Journal of Software, 2024, 35(8): 3897-3922. | |

| [2] | YILMAZ F M, YILDIZTEPE E. Statistical evaluation of deep learning models for stock return forecasting[J]. Computational Economics, 2024, 63(1): 221-244. |

| [3] | 王泉,陆啟想,施珮. 用于交通流量预测的多图扩散注意力网络[J]. 计算机应用, 2025, 45(5): 1472-1479. |

| WANG Q, LU Q X, SHI P. Multi-graph diffusion attention network for traffic flow prediction[J]. Journal of Computer Applications, 2025, 45(5): 1472-1479. | |

| [4] | JIANG J, HAN C, ZHAO W X, et al. PDFormer: propagation delay-aware dynamic long-range Transformer for traffic flow prediction[C]// Proceedings of the 37th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2023: 4365-4373. |

| [5] | 赵文竹,袁冠,张艳梅,等. 多视角融合的时空动态GCN城市交通流量预测[J]. 软件学报, 2024, 35(4): 1751-1773. |

| ZHAO W Z, YUAN G, ZHANG Y M, et al. Multi-view fused spatial-temporal dynamic GCN for urban traffic flow prediction[J]. Journal of Software, 2024, 35(4): 1751-1773. | |

| [6] | LI Y, WU K, LIU J. Self-paced ARIMA for robust time series prediction[J]. Knowledge-Based Systems, 2023, 269: No.110489. |

| [7] | SAPNKEN F E, KHALILI TAZEHKANDGHESHLAGH A, SALOMON DIBOMA B, et al. A whale optimization algorithm-based multivariate exponential smoothing grey-holt model for electricity price forecasting[J]. Expert Systems with Applications, 2024, 255(Pt B): No.124663. |

| [8] | LIU Q, LI F, WANG W. Memory augmented echo state network for time series prediction[J]. Neural Computing and Applications, 2024, 36(7): 3761-3776. |

| [9] | PENG P, CHEN Y, LIN W, et al. Attention-based CNN-LSTM for high-frequency multiple cryptocurrency trend prediction[J]. Expert Systems with Applications, 2024, 237(Pt B): No.121520. |

| [10] | TREBING K, MEHRKANOON S. Wind speed prediction using multidimensional convolutional neural networks[C]// Proceedings of the 2020 Symposium Series on Computational Intelligence. Piscataway: IEEE, 2020: 713-720. |

| [11] | ZHOU H, ZHANG S, PENG J, et al. Informer: beyond efficient Transformer for long sequence time-series forecasting[C]// Proceedings of the 35th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2021: 11106-11115. |

| [12] | WU H, XU J, WANG J, et al. Autoformer: decomposition Transformers with auto-correlation for long-term series forecasting[C]// Proceedings of the 35th International Conference on Neural Information Processing Systems. Red Hook: Curran Associates Inc., 2021: 22419-22430. |

| [13] | ZHANG Y, YAN J. Crossformer: Transformer utilizing cross-dimension dependency for multivariate time series forecasting [EB/OL]. [2025-05-20].. |

| [14] | LIN S, LIN W, WU W, et al. SegRNN: segment recurrent neural network for long-term time series forecasting[EB/OL]. [2025-05-20].. |

| [15] | LUO D, WANG X. ModernTCN: a modern pure convolution structure for general time series analysis[EB/OL]. [2025-05-20].. |

| [16] | 吴俊衡,王晓东,何启学. 基于统计分布感知与频域双通道融合的时序预测模型[J]. 计算机应用, 2026, 46(1): 113-123. |

| WU J H, WANG X D, HE Q X. Time series prediction model based on statistical distribution sensing and frequency domain dual-channel fusion[J]. Journal of Computer Applications, 2026, 46(1): 113-123. | |

| [17] | DENG J, CHEN X, JIANG R, et al. ST-Norm: spatial and temporal normalization for multi-variate time series forecasting[C]// Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery and Data Mining. New York: ACM, 2021: 269-278. |

| [18] | KIM T, KIM J, TAE Y, et al. Reversible instance normalization for accurate time-series forecasting against distribution shift [EB/OL]. [2025-05-20].. |

| [19] | FAN W, WANG P, WANG D, et al. Dish-TS: a general paradigm for alleviating distribution shift in time series forecasting[C]// Proceedings of the 37th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2023: 7522-7529. |

| [20] | BAHDANAU D, CHO K, BENGIO Y. Neural machine translation by jointly learning to align and translate[EB/OL]. [2025-04-12].. |

| [21] | VASWANI A, SHAZEER N, PARMAR N, et al. Attention is all you need[C]// Proceedings of the 31st International Conference on Neural Information Processing Systems. Red Hook: Curran Associates Inc., 2017: 6000-6010. |

| [22] | YANG Y, LV H, CHEN N. A survey on ensemble learning under the era of deep learning[J]. Artificial Intelligence Review, 2023, 56(6): 5545-5589. |

| [23] | 徐晓芳,管瑞. 基于神经网络集成学习算法的金融时间序列预测[J]. 计算机系统应用, 2022, 31(6): 29-37. |

| XU X F, GUAN R. Financial time series forecasting based on neural network ensemble learning algorithms[J]. Computer Systems and Applications, 2022, 31(6): 29-37. | |

| [24] | 李斌,刘全. 基于最小二乘的双权重学习法[J]. 计算机科学, 2020, 47(12): 210-217. |

| LI B, LIU Q. Double weighted learning algorithm based on least squares[J]. Computer Science, 2020, 47(12): 210-217. | |

| [25] | HU X, TANG X, ZHANG Q, et al. Combined machine learning forecasting method for short-term power load based on the dynamic weight adjustment [J]. Energy Reports, 2023, 9(S7): 866-873. |

| [26] | ADHIKARI R, VERMA G. Time series forecasting through a dynamic weighted ensemble approach[C]// Proceedings of the 3rd International Conference on Advanced Computing, Volume 1. New Delhi: Springer, 2015: 455-465. |

| [27] | ZENG A, CHEN M, ZHANG L, et al. Are Transformers effective for time series forecasting?[C]// Proceedings of the 37th AAAI Conference on Artificial Intelligence. Palo Alto: AAAI Press, 2023: 11121-11128. |

| [28] | NIE Y, NGUYEN N H, SINTHONG P, et al. A time series is worth 64 words: long-term forecasting with Transformers[EB/OL]. [2025-06-22].. |

| [29] | LIU Y, HU T, ZHANG H, et al. iTransformer: inverted Transformers are effective for time series forecasting[EB/OL]. [2024-10-05].. |

| [30] | WU H, HU T, LIU Y, et al. TimesNet: temporal 2D-variation modeling for general time series analysis[EB/OL]. [2025-05-20].. |

| [31] | YE H, CHEN J, GONG S, et al. ATFNet: adaptive time-frequency ensembled network for long-term time series forecasting[EB/OL]. [2025-04-06].. |

| [32] | ZHANG Y F, WEN Q, WANG X, et al. OneNet: enhancing time series forecasting models under concept drift by online ensembling [C]// Proceedings of the 37th International Conference on Neural Information Processing Systems. Red Hook: Curran Associates Inc., 2023: 69949-69980. |

| [1] | Wenjun FENG, Xinwei SONG, Yuntao YUE. Time series prediction of environmental electric field intensity with generalized correlation entropy loss function-based Transformer model [J]. Journal of Computer Applications, 2026, 46(6): 1872-1880. |

| [2] | Maozu GUO, Qingyu ZHANG, Lingling ZHAO, Yang DENG. Probabilistic structural damage identification based on hypersphere ring description [J]. Journal of Computer Applications, 2026, 46(6): 2016-2025. |

| [3] | Xing SHENG, Sunxian WENG, Kuosong CHEN, Zhongping WANG, Ruifeng REN, Yong LIU. Deep learning-based patent value evaluation for power grid enterprises [J]. Journal of Computer Applications, 2026, 46(5): 1468-1474. |

| [4] | Ruirui SONG, Leichun WANG, Yunping HE, Jinxiang WEI, Xiangfeng LU, Xiaomeng LIU. Long time series prediction based on hybrid self-attention and differentiated normalization [J]. Journal of Computer Applications, 2026, 46(5): 1499-1506. |

| [5] | Xingcan LI, Lizhong DING, Junyu ZHANG, Chunhui ZHANG. ContraStacker: an ensemble approach for extremely imbalanced fraud detection [J]. Journal of Computer Applications, 2026, 46(5): 1363-1369. |

| [6] | Chi ZHANG, Xianjing MENG, Changhao DOU, Qian WANG, Leilei GENG, Xiaoming XI. MD-FVR: cascaded finger vein recognition network based on multi-domain feature fusion [J]. Journal of Computer Applications, 2026, 46(5): 1658-1666. |

| [7] | Yifan SUO, Songhua LIU, Qiuzhi HAO. Time series anomaly detection method based on high-order feature aggregation [J]. Journal of Computer Applications, 2026, 46(4): 1131-1138. |

| [8] | Jing ZHANG, Songhua LIU, Yuanqian ZHU. Time series representation method based on spectral sensing and hierarchical convolution [J]. Journal of Computer Applications, 2026, 46(4): 1124-1130. |

| [9] | Chuandong QIN, Zhiqiang SUO. Skin cancer classification integrating improved ResNet50 with ensemble classifier [J]. Journal of Computer Applications, 2026, 46(4): 1354-1362. |

| [10] | Chunyong YIN, Bufan ZHANG. Multi-scale based multivariate time series anomaly detection model [J]. Journal of Computer Applications, 2026, 46(3): 790-797. |

| [11] | Yuebo FAN, Mingxuan CHEN, Xian TANG, Yongbin GAO, Wenchao LI. Multi-dimensional frequency domain feature fusion for human-object interaction detection [J]. Journal of Computer Applications, 2026, 46(2): 580-586. |

| [12] | Rifeng ZHANG, Guangming LI, Yurong OUYANG. Low-light image enhancement network guided by reflection prior map [J]. Journal of Computer Applications, 2026, 46(2): 546-554. |

| [13] | Hanyue WEI, Chenjuan GUO, Jieyuan MEI, Jindong TIAN, Peng CHEN, Ronghui XU, Bin YANG. MATCH: multimodal stock prediction framework integrating time-frequency features and hybrid text [J]. Journal of Computer Applications, 2026, 46(2): 427-436. |

| [14] | Junheng WU, Xiaodong WANG, Qixue HE. Time series prediction model based on statistical distribution sensing and frequency domain dual-channel fusion [J]. Journal of Computer Applications, 2026, 46(1): 113-123. |

| [15] | Xiang WANG, Zhixiang CHEN, Guojun MAO. Multivariate time series prediction method combining local and global correlation [J]. Journal of Computer Applications, 2025, 45(9): 2806-2816. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||